Regulatory Risk in Digital Assets: What Firms Must Know

Regulatory risk in digital assets is defined as the potential for adverse operational, financial, or reputational harm caused by changes in laws, enforcement priorities, or legal classifications affecting digital asset firms. This risk applies even to firms currently in full compliance, because a regulatory reclassification or a new enforcement directive can instantly transform a lawful activity into a violation. The SEC, the Financial Action Task Force (FATF), and the EU’s Markets in Crypto-Assets Regulation (MiCA) each impose distinct obligations that can conflict across jurisdictions. For finance and legal professionals, understanding regulatory risk is not an academic exercise. It is the foundation of every defensible compliance program in the digital asset space.

What is regulatory risk in digital assets?

Regulatory risk in digital assets is the threat that changing laws or enforcement disrupt operations, trigger financial penalties, or damage an organization’s reputation, even when the firm was compliant at the time of the activity. This definition captures something traditional compliance frameworks often miss: the risk is not static. It moves with the regulatory environment, not with the firm’s conduct.

Three structural features make digital asset regulatory risk uniquely difficult to manage. First, classification ambiguity means the same token can be a security under U.S. federal law, a commodity under CFTC jurisdiction, or an e-money instrument under the UK Financial Conduct Authority (FCA). Second, jurisdictional fragmentation means a single cross-border transaction can trigger compliance obligations in multiple legal systems simultaneously. Third, enforcement variability means that regulatory bodies shift their priorities, and firms that were tolerated yesterday face formal action today.

The practical consequences are concrete. A firm operating a token issuance program may face SEC enforcement if the token is reclassified as a security under the Howey test, even if it was structured as a utility token at launch. A virtual asset service provider (VASP) operating across the EU and the UK faces parallel authorization requirements under MiCA and the FCA’s CP26/13 consultation framework, with no automatic mutual recognition between them.

Pro Tip: Map your firm’s entire product and transaction footprint against the regulatory perimeter of each jurisdiction you touch before assuming your current structure is compliant.

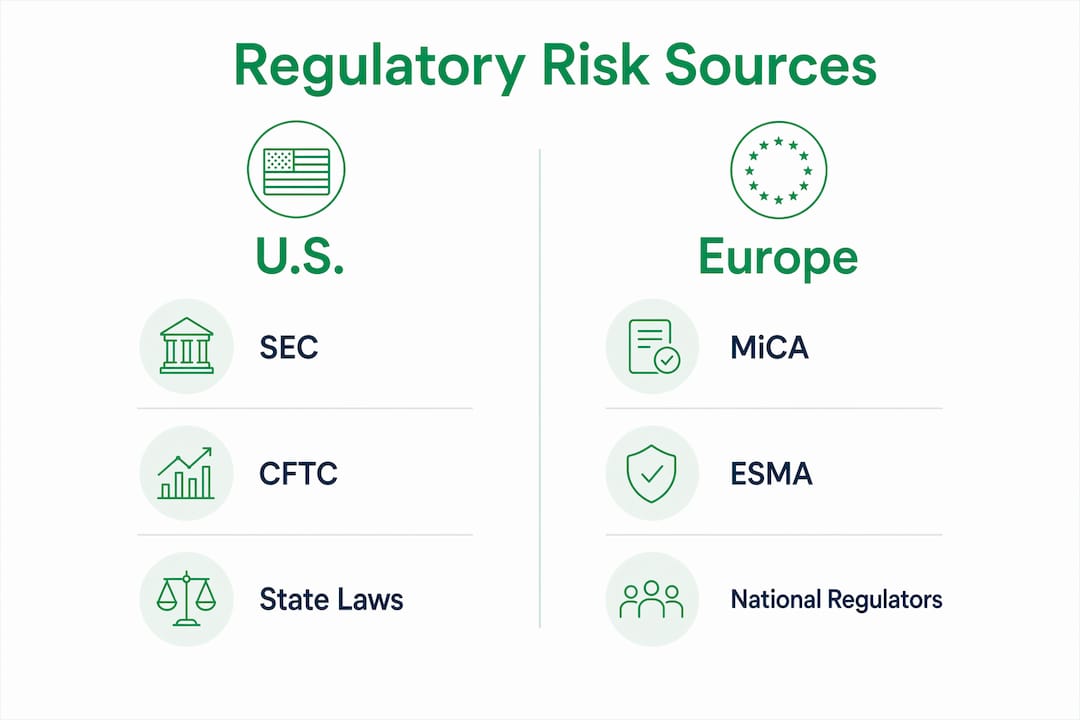

What are the primary sources of regulatory risk for digital assets?

The sources of regulatory risk in digital assets fall into four categories, each with distinct compliance implications.

-

Classification uncertainty. The same digital asset may be treated as a security, commodity, or e-money depending on jurisdiction and token attributes. This creates overlapping compliance regimes and multiplies the cost of cross-border activity. The SEC’s Project Crypto initiative is actively working to clarify how federal securities laws apply to crypto assets, but the process is ongoing and enforcement actions continue in parallel.

-

Jurisdictional fragmentation. The U.S. operates under a split SEC/CFTC model. The EU applies MiCA as a unified framework. The UK is developing its own post-Brexit regime through the FCA. Singapore, Hong Kong, and the UAE each maintain separate licensing regimes. A firm active in three jurisdictions may face three entirely different authorization processes, capital requirements, and disclosure obligations.

-

AML/CFT compliance pressure. FATF Recommendation 15 extends anti-money laundering and counter-terrorist financing obligations to VASPs, requiring risk-based supervision, licensing, and Travel Rule compliance with a USD/EUR 1,000 threshold. VASPs must apply due diligence controls equivalent to those of traditional financial institutions, a standard that many digital asset firms are not yet operationally equipped to meet.

-

Enforcement variability. Regulatory bodies shift focus without advance notice. The SEC’s Project Crypto signals a more structured approach to crypto classification, but enforcement actions against exchanges, token issuers, and DeFi protocols have continued throughout 2025 and 2026. BaFin’s action against Ethena in Germany illustrates how national regulators within the EU can act independently even under a harmonized framework like MiCA.

The U.S. CLARITY Act, currently progressing through Congress, attempts to resolve the SEC/CFTC jurisdictional split by establishing clearer criteria for when a digital asset is a commodity versus a security. Until it passes, firms must manage the ambiguity directly.

Pro Tip: Treat regulatory fragmentation as a permanent operating condition, not a temporary gap. Build jurisdiction-specific compliance modules into your program architecture from day one.

How does legal classification shape digital asset compliance obligations?

Legal classification is the single most consequential variable in digital asset regulatory risk. The applicable regulatory regime, and therefore the entire compliance obligation set, follows directly from how a token is classified.

The table below compares the three major regulatory frameworks and their classification approaches:

| Jurisdiction | Regulator | Classification approach | Key obligations triggered |

|---|---|---|---|

| United States | SEC / CFTC | Howey test for securities; commodity status for Bitcoin and Ether | Registration, disclosure, broker-dealer licensing |

| European Union | ESMA / national NCAs | MiCA categories: asset-referenced tokens, e-money tokens, other crypto-assets | Authorization, whitepaper publication, reserve requirements |

| United Kingdom | FCA | Financial promotions regime; evolving token taxonomy under CP26/13 | Registration, financial promotion approval, AML controls |

The SEC applies the Howey test to determine whether a crypto asset is a security, which triggers the full weight of federal securities law including registration, disclosure, and anti-fraud provisions. A token that fails the Howey test at launch but later develops secondary market trading characteristics may be reclassified, exposing the issuer retroactively.

Under MiCA, the classification of a token as an asset-referenced token or an e-money token triggers reserve requirements, redemption rights, and capital adequacy obligations that do not apply to other crypto-assets. This distinction has significant balance sheet implications for treasury teams and legal advisors structuring stablecoin products.

Governance and disclosure misalignment can reintroduce securities characterization risk even for protocols that were initially structured to avoid it. If a decentralized protocol’s actual decision-making is concentrated in a founding team, and that reality is not reflected in public disclosures, the SEC may treat the token as a security regardless of its technical architecture.

Pro Tip: Conduct a classification stress test annually. Apply the Howey test, the MiCA taxonomy, and the FCA’s evolving criteria to each token or product in your portfolio, and document the analysis with legal counsel.

What compliance strategies reduce regulatory risk in digital assets?

Managing digital asset compliance issues requires a structured program that goes beyond minimum regulatory requirements. The following steps define a defensible approach:

-

Build a risk-based compliance program aligned with FATF Recommendation 15. This means conducting a documented risk assessment of your VASP activities, identifying high-risk customer segments and transaction types, and calibrating controls proportionally. A one-size-fits-all AML program fails both regulators and auditors.

-

Implement Travel Rule controls with KYVASP mapping. Travel Rule compliance requires more than wallet address parsing. Firms need jurisdiction-aware workflows that identify the counterparty VASP, verify its regulatory status, and transmit required originator and beneficiary data. Technical limitations mean that address-based identification alone is insufficient.

-

Prepare for the MiCA July 2026 authorization cliff. MiCA requires crypto-asset service providers to obtain authorization by July 1, 2026, after which non-compliance can result in penalties up to €15 million or 5% of annual turnover. Grandfathering provisions expire on that date. Firms that have not completed their authorization process need wind-down playbooks and client asset segregation plans as contingency measures.

-

Coordinate compliance across jurisdictions. Regulatory fragmentation creates friction for cross-border firms. Assign jurisdiction owners within your compliance team, maintain a regulatory change log by market, and establish escalation protocols when a new rule in one jurisdiction conflicts with an existing obligation in another.

-

Deploy transaction monitoring technology calibrated to digital asset risk. Traditional AML transaction monitoring systems are not designed for blockchain data. Tools that incorporate on-chain analytics, counterparty risk scoring, and real-time Travel Rule data exchange are necessary to meet the standard that regulators now expect of VASPs.

-

Align governance and disclosure with operational reality. Disclosure alignment reduces the risk that a regulator characterizes your token or protocol as a security based on the actual distribution of control. Legal teams should review whitepapers, governance documentation, and marketing materials together, not in isolation.

How do global regulatory developments affect the compliance outlook?

The global regulatory environment for digital assets is converging toward stricter oversight, but the pace and structure of that convergence vary significantly by region.

- MiCA is the most comprehensive framework currently in force, covering the EU’s 27 member states with a single authorization regime. Its July 2026 cliff is the most immediate operational deadline for any firm with EU exposure.

- The U.S. CLARITY Act proposes to resolve the SEC/CFTC jurisdictional split by defining when a digital asset is a commodity versus a security based on the degree of decentralization. Its passage would materially reduce classification uncertainty for U.S.-based issuers and exchanges.

- The UK’s CP26/13 consultation signals the FCA’s intent to build a comprehensive crypto regulatory regime, including stablecoin authorization, exchange licensing, and lending rules. Firms operating in the UK should treat this as an active compliance planning horizon, not a future concern.

- FATF updates continue to tighten VASP supervision standards globally. Countries that fail to implement FATF recommendations face grey-listing, which directly affects the correspondent banking relationships and payment rails that digital asset firms depend on.

The operational readiness required to meet these deadlines includes not just legal authorization but migration projects, client notification programs, and contingency planning for scenarios where authorization is delayed. Firms that treat regulatory deadlines as legal events rather than operational projects consistently underestimate the lead time required.

Key takeaways

Regulatory risk in digital assets is a dynamic, multi-jurisdictional threat that requires classification analysis, jurisdiction-specific compliance programs, and continuous monitoring of enforcement trends to manage effectively.

| Point | Details |

|---|---|

| Classification drives obligations | How a token is classified under SEC, MiCA, or FCA rules determines every compliance requirement that follows. |

| FATF Recommendation 15 is the AML baseline | VASPs must apply risk-based AML/CFT controls and Travel Rule compliance equivalent to traditional financial institutions. |

| MiCA’s July 2026 deadline is operational | Authorization by July 1, 2026 is required; penalties reach €15 million or 5% of turnover for non-compliant firms. |

| Fragmentation requires local compliance modules | Cross-border firms cannot apply a single compliance program across the U.S., EU, and UK without jurisdiction-specific adaptation. |

| Governance alignment reduces securities risk | Disclosure and governance documentation must reflect operational reality to avoid unintended securities characterization. |

The compliance trap most firms don’t see coming

Most firms I work with treat regulatory risk as a legal department problem. They commission a classification opinion, file the opinion in a folder, and move on. That approach fails for one specific reason: classification is not a one-time event. It is a continuous condition that changes as your product evolves, as secondary markets develop, and as regulators publish new guidance.

The firms that manage regulatory risk well do something different. They embed compliance review into product development cycles, not just at launch but at every material feature change. They treat the 2026 compliance readiness calendar as an operational project with owners, milestones, and contingency plans. They also invest in governance documentation that reflects how decisions are actually made, not how the whitepaper says they should be made.

The uncomfortable truth is that the firms most exposed to regulatory risk are often the ones that believe they have already solved it. A classification opinion from 2023 does not account for Project Crypto, the MiCA authorization cliff, or the FCA’s evolving CP26/13 framework. Regulatory risk management is not a destination. It is a standing function that requires the same rigor as financial reporting.

— Gregg

How DARE helps firms manage digital asset regulatory risk

Wush built the Digital Asset Readiness Evaluation (DARE) specifically for finance and legal professionals who need more than a static compliance checklist. DARE provides a structured certification framework that covers classification analysis, AML/CFT program design, governance alignment, and operational readiness across the major regulatory regimes including MiCA, FATF, and SEC requirements. The platform’s modular assessments map directly to the compliance obligations that matter most in 2026, and the annual renewal process keeps your certification current as regulations evolve. If your firm is managing digital asset regulatory exposure and needs a credentialed framework to demonstrate readiness to regulators, counterparties, and boards, DARE is the structured path forward.

FAQ

What is regulatory risk in digital assets?

Regulatory risk in digital assets is the potential for harm caused by changes in laws, enforcement actions, or legal classifications that affect digital asset firms, even when those firms are currently compliant. It arises from classification ambiguity, jurisdictional fragmentation, and shifting enforcement priorities across bodies like the SEC, FATF, and EU regulators.

What is regulatory safe harbor for digital assets?

A regulatory safe harbor for digital assets is a defined legal provision that protects firms from enforcement action when they meet specified conditions, such as disclosure standards or decentralization thresholds. The U.S. CLARITY Act proposes safe harbor provisions that would shield token issuers from securities law liability during a defined development period.

How do regulations affect digital assets operationally?

Regulations affect digital assets by imposing authorization requirements, capital standards, disclosure obligations, and AML/CFT controls that directly shape product design, custody arrangements, and transaction processing. MiCA’s July 2026 authorization deadline, for example, requires firms to complete operational migration projects, not just legal filings.

What is the Travel Rule and why does it matter for VASPs?

The Travel Rule, established under FATF Recommendation 15, requires VASPs to transmit originator and beneficiary information for transactions above USD/EUR 1,000. Compliance requires KYVASP mapping and jurisdiction-aware workflows because wallet address parsing alone cannot identify the counterparty VASP.

How can firms reduce digital asset compliance risk across jurisdictions?

Firms reduce cross-jurisdictional compliance risk by building jurisdiction-specific compliance modules, assigning regulatory owners by market, and maintaining a live regulatory change log. Aligning governance documentation with operational reality and deploying on-chain transaction monitoring tools are equally critical components of a defensible program.