Digital Asset Regulatory Exposure: What You Need to Know

What is digital asset regulatory exposure? For most compliance teams, it is far broader than managing a few cryptocurrency positions. It covers every point where your institution touches a digital asset transaction, whether as a custodian, broker, exchange operator, or technology provider, and every obligation that contact creates under an increasingly dense web of law. In 2026, that web now spans the U.S. Digital Asset Market Clarity Act, new IRS broker reporting rules, and Australia’s freshly enacted licensing regime. The firms that get ahead of this are the ones that treat regulatory exposure as a structural risk, not a technology problem.

Table of Contents

- Key takeaways

- What digital asset regulatory exposure actually means

- U.S. regulatory changes defining exposure in 2026

- Australian regulatory reforms and their compliance impact

- Key compliance risks in managing digital asset exposure

- How to navigate regulatory exposure: practical steps

- My perspective on the real challenge here

- Get certified for digital asset compliance readiness

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Exposure is broader than tokens | Regulatory obligations fall on intermediaries like brokers, custodians, and exchanges, not just the assets themselves. |

| 2026 rules created new obligations | U.S. and Australian reforms add licensing, reporting, and AML requirements that demand immediate compliance program updates. |

| Chain-hopping is a live threat | Traditional AML tools cannot detect cross-chain laundering without specialized blockchain analytics. |

| Jurisdictional overlap compounds risk | A token’s classification can shift across borders, creating sudden legal obligations for international firms. |

| Governance must reach the board | Effective oversight of digital asset regulatory exposure requires board-level accountability, not just operational controls. |

What digital asset regulatory exposure actually means

Regulatory exposure, at its core, is the total set of legal and compliance obligations an institution carries because of its involvement with digital assets. The phrase sounds narrow. It is not.

The assets covered are wider than Bitcoin and Ether. Regulatory regimes increasingly address:

- Cryptocurrencies and stablecoins used for payment or investment

- Non-fungible tokens (NFTs) where they function as securities or financial instruments

- Tokenized securities that replicate traditional asset ownership on-chain

- DeFi protocol interactions where smart contracts substitute for intermediary functions

The intermediaries exposed are equally broad. Most impactful regulations focus on entities intermediating money rather than on the crypto asset itself, which means brokers, custodians, exchanges, kiosk operators, and even real estate professionals who facilitate certain digital asset transactions all carry direct compliance obligations.

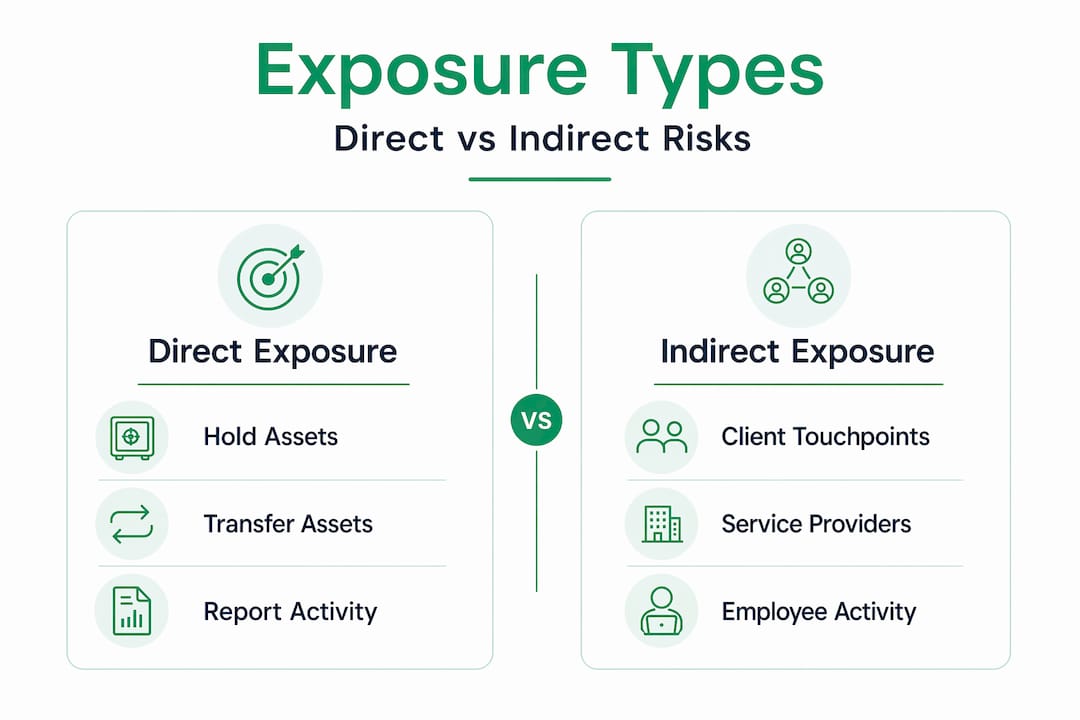

Direct exposure occurs when your institution holds, transfers, or reports on digital assets. Indirect exposure is subtler. A correspondent banking relationship with a crypto exchange, or a treasury investment in a tokenized money market fund, creates obligations you may not have mapped. Cross-chain risks add another layer: a transaction that starts on Ethereum and ends on a privacy chain may pass through your compliance perimeter without triggering standard monitoring alerts.

Understanding digital asset regulation therefore starts with mapping every touchpoint, not just the ones that look like obvious crypto activity.

U.S. regulatory changes defining exposure in 2026

The legislative and regulatory activity in the United States in 2026 has materially changed what compliance means for any institution touching digital assets.

The Digital Asset Market Clarity Act is the most significant development. It extends Bank Secrecy Act requirements fully to digital asset intermediaries, mandating AML and CFT programs, sanctions compliance, risk-based examinations, mandatory use of blockchain analytics, and formal registration for crypto kiosk operators. This is not an extension of existing guidance. It is a statutory floor.

| Requirement | Who it affects | Compliance implication |

|---|---|---|

| BSA program obligations | All digital asset intermediaries | Formal AML/CFT policies required |

| IRS Form 1099-DA reporting | Brokers, including real estate professionals | Gross proceeds reported since 2025; basis since 2026 |

| Crypto kiosk registration | Kiosk operators | Federal registration now mandatory |

| Special Measure 6 authority | Treasury, affecting international exposure | Enables action against foreign jurisdictions with digital asset money laundering risk |

| Blockchain analytics mandate | All covered intermediaries | Real-time on-chain monitoring required |

The IRS reporting change deserves specific attention. Basis reporting on Form 1099-DA began in 2026, which means brokers must now track cost basis across wallets and transactions, including for clients who have moved assets across multiple platforms. The operational lift is substantial and the liability for errors is real.

The CLARITY Act also creates Special Measure 6 authority for Treasury, allowing it to designate foreign jurisdictions as primary money laundering concerns in the digital asset context. For institutions with any cross-border crypto exposure, this means sanctions screening must now account for jurisdiction-level risk, not just individual counterparty risk.

Pro Tip: Map your institution’s crypto touchpoints against the CLARITY Act’s intermediary definitions before your next examination. Examiners will be asking whether your AML program was updated to reflect statutory obligations, and “we’re monitoring developments” is no longer an acceptable answer.

Australian regulatory reforms and their compliance impact

Australia’s approach to digital asset regulatory exposure took a decisive turn in 2026. The Corporations Amendment (Digital Assets Framework) Act 2026 integrates digital asset platforms into the existing Australian Financial Services License regime, with full effect from April 2027.

The Act introduces two key categories. Digital Asset Platforms (DAPs) cover entities that hold or exchange digital assets on behalf of clients. Tokenised Custody Platforms (TCPs) cover those that provide custody of tokenized representations of traditional assets. Both categories must now comply with licensing, disclosure, conduct, and dispute resolution obligations that mirror existing AFSL requirements.

| Platform type | Definition | Key obligation |

|---|---|---|

| Digital Asset Platform (DAP) | Holds or exchanges digital assets for clients | AFSL licensing, client disclosure, conduct rules |

| Tokenised Custody Platform (TCP) | Custodies tokenized traditional assets | AFSL licensing, custody standards, dispute resolution |

| Transitional entities | Operating before April 2027 | ASIC no-action position until June 30, 2026 |

The dual obligation structure is where Australian firms face the most complexity. Digital asset platforms must comply with both the AFSL regime and the existing AML/CTF framework administered by AUSTRAC. These are not identical. AML/CTF obligations under AUSTRAC apply at the point of registration, while AFSL conduct obligations apply to how you interact with clients. A platform that satisfies one regime’s requirements does not automatically satisfy the other.

For international firms with Australian operations or Australian client exposure, the April 2027 effective date is not a distant deadline. Licensing applications, systems upgrades, and policy rewrites take time. Firms reviewing their Australian compliance positioning now will be far better placed than those waiting for ASIC to issue further guidance.

Key compliance risks in managing digital asset exposure

The operational reality of managing digital asset compliance risks is considerably harder than the regulatory text suggests. Three categories of risk stand out above the others.

AML and transaction monitoring gaps. Traditional AML and KYC tools are insufficient when dealing with chain-hopping, nested services, and DeFi protocols. Chain-hopping is the practice of moving funds across multiple blockchains to obscure origin. Nested services are exchanges operating within other exchanges, making beneficial ownership nearly impossible to trace without blockchain analytics. Standard rule-based transaction monitoring simply does not see these patterns.

Sanctions screening inadequacy. Typology-driven on-chain analysis is now a baseline expectation, not a best practice. Traditional SDN list screening catches designated wallets. It does not catch funds that passed through those wallets two transactions ago, or stablecoins issued by prohibited entities but held through intermediaries. The indirect exposure risk here is significant and frequently underestimated.

Employee and personal wallet exposure. This is arguably the fastest-growing compliance blind spot. Employee wallet activity and DeFi participation can create outside business interest issues, conflict of interest violations, and direct regulatory exposure for the firm. Most compliance programs have no policy covering this.

Additional risks worth active monitoring:

- Fragmented token classifications across jurisdictions, where shifting token functions or legal status can abruptly change which regulatory regime applies

- DeFi protocol governance tokens that may qualify as securities in some jurisdictions

- Real-time reporting obligations that cannot be met with batch-processing infrastructure

Pro Tip: Run a gap analysis specifically on employee digital asset activity. Ask whether your current personal account dealing policy covers DeFi wallets, NFT activity, and participation in token governance votes. Most policies written before 2024 are silent on all three.

How to navigate regulatory exposure: practical steps

Building a defensible compliance framework for digital asset regulatory exposure does not require starting from scratch. Existing AML and BSA frameworks can be adapted using blockchain ledger data as the primary input, which means your existing risk-based approach remains the foundation.

-

Conduct a regulatory mapping exercise. Identify every point where your institution touches digital assets and map each touchpoint to the applicable regulatory regime. Include indirect exposure through correspondent relationships and third-party technology providers.

-

Implement blockchain analytics at the wallet level. Wallet-level monitoring and fund flow tracing across chains are now the baseline for detecting laundering, sanctions evasion, and fraud. Select a tool that covers multiple blockchains and provides real-time alerts, not end-of-day batch reports.

-

Update KYC, transaction monitoring, and reporting procedures. Embed 2026 regulatory changes, including CLARITY Act obligations and IRS Form 1099-DA requirements, into existing workflows. Do not treat these as separate compliance streams.

-

Establish board-level oversight. Review your board oversight framework for digital assets specifically. Directors need enough understanding of digital asset risk to ask the right questions, even if they do not need technical blockchain expertise.

-

Train compliance staff on digital asset typologies. Chain-hopping, mixer usage, NFT wash trading, and DeFi governance risks require specialized training that most general AML programs do not cover. Invest in it before the next examination cycle.

-

Coordinate cross-border compliance positions. Where your institution operates in multiple jurisdictions, assign clear ownership for each regulatory regime. The intersection of U.S. CLARITY Act obligations and Australian AFSL requirements, for example, requires deliberate coordination rather than parallel workstreams.

My perspective on the real challenge here

I have watched compliance teams make the same mistake repeatedly: they treat digital asset regulatory exposure as a discrete project rather than a permanent feature of the risk environment. They hire a specialist, update one policy, and consider the matter handled. Then a new regulation arrives, or a transaction pattern shifts, and they are back at square one.

What I have found actually works is treating digital asset compliance the same way you treat AML model validation: as an ongoing discipline with scheduled reviews, not a one-time remediation. The firms that are genuinely ahead of this are not the ones that spent the most on technology. They are the ones that invested in building internal expertise and governance structures that can absorb regulatory change without panic.

The other thing I would push back on is the instinct to wait for regulatory certainty before acting. Certainty is not coming. Overlapping jurisdictional rules and shifting token classifications are a permanent feature of this space, not a transitional problem. The compliance leaders doing the best work right now have accepted ambiguity as a given and built flexible frameworks accordingly. Rigidity is the real risk here, not the regulations themselves.

— Gregg

Get certified for digital asset compliance readiness

Managing digital asset regulatory exposure at the level 2026 demands requires more than policy updates. It requires structured, credentialed expertise that your institution can point to during examinations and audits.

Wush offers the Digital Asset Readiness Evaluation (DARE), a certification program built specifically for finance and compliance professionals navigating the governance gap in enterprise digital asset operations. DARE covers custody, AML, sanctions, regulatory compliance, and operational controls through modular learning and formal assessment. Credentials are blockchain-backed and renewed annually to reflect evolving regulatory standards. If your team needs to demonstrate compliance readiness ahead of the next examination cycle, DARE is the structured path to get there.

FAQ

What is digital asset regulatory exposure?

Digital asset regulatory exposure is the total set of legal and compliance obligations an institution carries because of its direct or indirect involvement with digital assets. It encompasses AML, sanctions, tax reporting, licensing, and conduct obligations triggered by any touchpoint with digital asset transactions or intermediaries.

Which regulations define digital asset exposure in the U.S. in 2026?

The Digital Asset Market Clarity Act and IRS Form 1099-DA reporting rules are the primary drivers in 2026. The CLARITY Act extends Bank Secrecy Act requirements to all digital asset intermediaries, while IRS rules now require brokers to report both gross proceeds and cost basis.

What are the biggest digital asset compliance risks for financial institutions?

The three highest-priority risks are AML gaps from chain-hopping and nested services, sanctions screening failures from indirect exposure through complex crypto networks, and employee-related exposure from personal wallet and DeFi activity that most compliance programs do not currently address.

How does Australia’s 2026 digital asset framework affect compliance teams?

Australia’s Corporations Amendment (Digital Assets Framework) Act 2026 requires Digital Asset Platforms and Tokenised Custody Platforms to hold an Australian Financial Services License from April 2027. Firms must satisfy both AFSL conduct obligations and AUSTRAC AML/CTF requirements, which are distinct and do not automatically satisfy each other.

How can firms start to manage digital asset regulatory exposure?

Start with a regulatory mapping exercise that covers every digital asset touchpoint, including indirect exposure through third parties. Then update your blockchain analytics capability to wallet-level monitoring, revise KYC and transaction monitoring procedures to reflect 2026 rules, and establish formal board-level oversight of digital asset risk.