Executive Digital Asset Due Diligence Guide for Finance Leaders

Executive digital asset due diligence is the systematic process of evaluating digital assets across regulatory, operational, technical, and financial dimensions before committing capital or governance resources. In 2026, this process has become a specialized discipline in its own right, distinct from traditional investment due diligence. Frameworks like the SBAI crypto operational due diligence template, custody providers like Coinbase Custody, and compliance standards including KYC/AML requirements have raised the bar for what thorough evaluation looks like. The collapse of major crypto entities in recent years made clear that bolting crypto-specific questions onto legacy hedge fund questionnaires is not a substitute for purpose-built digital asset assessment. Finance executives who treat this as a checkbox exercise expose their organizations to custody failures, regulatory sanctions, and valuation errors that are difficult to reverse.

What does an executive digital asset due diligence guide cover?

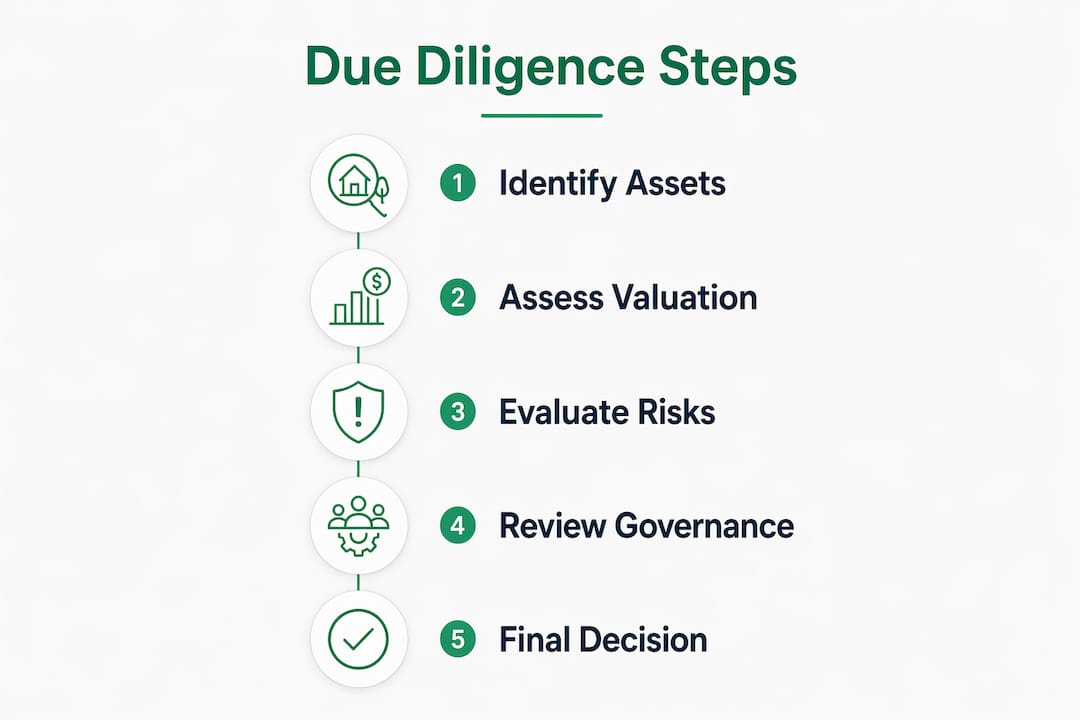

A rigorous digital asset due diligence process spans four core lanes: custody and key management, technology and smart contracts, regulatory exposure, and team and governance integrity. Each lane carries distinct risks that require dedicated assessment rather than a generalized review.

Custody and key management is where most institutional losses originate. Custody models range from institutional third-party custodians like Coinbase Custody, to self-custody with hardware wallets, to exchange custody, each with a fundamentally different risk profile. Institutional custodians are considered the gold standard for enterprise holdings because they offer proof-of-reserves reporting, segregated client assets, and insurance coverage. Exchange custody, by contrast, commingles assets and exposes the holder to counterparty risk. Any executive due diligence checklist must document which model is in use and verify the controls around it.

Technology and smart contract assessment requires reviewing audit history, blockchain consensus mechanisms, and upgrade governance. A 22-item due diligence checklist covering smart contracts, tokenomics, regulatory exposure, and team hygiene represents the minimum viable scope for early-stage digital asset review. For mature enterprise holdings, that scope expands considerably.

Regulatory exposure is the most dynamic lane in 2026. The SEC’s evolving stance on token classification, the EU’s Markets in Crypto-Assets regulation (MiCA), and jurisdictional fragmentation across Asia-Pacific all create compliance obligations that shift quarterly. Executives must map each asset to its applicable regulatory regime and document the legal opinion supporting that classification. For a detailed breakdown of current obligations, the 2026 compliance readiness analysis from Wush provides a current-state reference.

Team, treasury hygiene, and governance round out the checklist. Assess whether the asset’s governing entity publishes audited financials, whether token allocations are subject to vesting schedules, and whether governance votes are recorded on-chain. A comprehensive diligence framework uses 57 critical questions across seven categories including financial, legal, operational, and IT dimensions. That scope is appropriate for any significant digital asset position.

Pro Tip: Build your executive due diligence checklist in a shared workspace like Notion or Confluence so that legal, finance, and technology reviewers can contribute simultaneously rather than sequentially. Sequential reviews add weeks to a process that is already running longer than most executives expect.

| Category | Key assessment focus |

|---|---|

| Custody model | Third-party vs. self-custody; proof of reserves; asset segregation |

| Smart contracts | Audit history; upgrade governance; known vulnerabilities |

| Regulatory exposure | SEC classification; MiCA applicability; jurisdictional mapping |

| Team and governance | Vesting schedules; on-chain governance records; audited financials |

How to evaluate digital asset valuation and financial risks

Digital asset valuation is defined under ASC 820 and IFRS 13 as a fair value measurement based on exit price in the principal market. That sounds straightforward until you account for the fact that the same token trades at materially different prices across Binance, Kraken, and Coinbase simultaneously. Identifying the principal market, the venue with the highest volume and activity for that specific asset, is the first step before any price is recorded.

Traditional valuation approaches like discounted cash flow remain valid but require modification for crypto volatility and liquidity considerations. A modified DCF model for a yield-bearing token must account for emission schedules that dilute future cash flows, staking reward rates that fluctuate with network participation, and burn mechanisms that reduce supply over time. Each of these variables can shift a valuation by an order of magnitude, which is why static spreadsheet models are inadequate for digital assets.

Tokenomics analysis is not optional for any serious digital asset evaluation process. Executives must understand the total supply, circulating supply, unlock schedules for team and investor allocations, and the governance rights attached to the token. A token with 80% of supply locked in a team wallet that vests over 24 months carries a structural overhang that suppresses fair value relative to spot price. Valuation specialists integrate ASC 820 and IFRS 13 with blockchain data analytics and tokenomics to produce defensible valuations that regulators will accept.

Liquidity discounts are frequently underestimated. Tokens with thin order books, high bid-ask spreads, or concentrated ownership require a discount for lack of marketability that can range from 20% to 60% of spot price depending on position size. For a deeper framework on quantifying this exposure, Wush’s liquidity risk assessment guide walks through the specific metrics finance professionals should apply.

Pro Tip: Never rely on a single exchange’s price feed for valuation. Use a volume-weighted average price across at least three tier-one venues and document the methodology. Auditors and regulators will ask for it.

Which operational and compliance risks should executives prioritize?

Operational due diligence for digital assets is fundamentally different from traditional fund diligence. The non-custodial risks, wallet infrastructure complexity, and regulatory ambiguity create failure modes that have no equivalent in equity or fixed income portfolios. Executives who underestimate this difference make the most costly mistakes.

The highest-priority operational risks to assess are:

- Wallet infrastructure and key management. Multi-signature setups requiring multiple keyholders to authorize transactions are the minimum acceptable standard for institutional holdings. Single-key wallets controlled by one individual represent an unacceptable concentration of operational risk.

- KYC/AML compliance and transaction monitoring. Every counterparty in a digital asset transaction must be screened against OFAC, FinCEN, and applicable local sanctions lists. Continuous monitoring, not just onboarding checks, is required under current regulatory expectations.

- Third-party service provider credentials. Auditors, fund administrators, and legal counsel working in digital assets must have demonstrable crypto-specific experience. A Big Four firm with a dedicated digital assets practice is not equivalent to a generalist accounting firm that has reviewed one crypto client.

- Asset segregation verification. Client assets must be provably separate from the custodian’s or counterparty’s own holdings. Proof-of-reserves attestations from independent auditors are the current best practice, though they are not yet universally required.

- Insurance coverage. Confirm whether custody insurance covers hot wallet holdings, cold storage, and insider theft separately. Most policies have sublimits that executives do not read until after a loss event.

Red flags that should pause or terminate a diligence process include the absence of independent smart contract audits, unclear or undocumented asset segregation practices, legal counsel who cannot articulate the asset’s regulatory classification, and evasive or delayed responses to standard information requests. On that last point, sending questions in waves rather than a single batch is a proven technique for identifying hidden liabilities. Evasive or inconsistent answers across multiple rounds of inquiry are a stronger signal than any single red flag.

For executives building out their operational accountability frameworks, the governance structures around digital assets require the same rigor applied to any other enterprise risk category.

What are best practices for structuring the diligence process?

The due diligence process for complex transactions now takes 64% longer than it did a decade ago. For digital assets, that timeline extends further because of the technical complexity of blockchain verification, the pace of regulatory change, and the limited pool of qualified third-party reviewers. Starting preparation earlier than feels necessary is the single most effective time management decision an executive can make.

A structured digital asset evaluation process follows these stages:

- Scoping and preparation. Define the asset categories in scope, the regulatory jurisdictions involved, and the internal stakeholders required. Assign a lead for each of the four diligence lanes before any information requests go out.

- Wave one inquiry. Send an initial information request covering custody arrangements, regulatory status, and audited financials. Evaluate the completeness and speed of responses before proceeding.

- Technical and legal deep dive. Commission an independent smart contract audit if one does not exist or is more than 12 months old. Obtain a legal opinion on token classification under SEC and MiCA frameworks.

- Valuation and financial modeling. Apply the modified DCF and principal market analysis. Document all assumptions, discount rates, and tokenomics inputs.

- Wave two inquiry and gap resolution. Send follow-up questions targeting inconsistencies or gaps identified in the first wave. This stage frequently surfaces the most material risks.

- Final report and governance sign-off. Compile findings into a structured report with risk ratings by category. Present to the board or investment committee with explicit recommendations.

Pro Tip: Assign a dedicated diligence project manager who is not the decision-maker. Decision-makers under time pressure tend to compress stages two through five into a single meeting. That compression is where most diligence failures originate.

| Stage | Common pitfall | Mitigation |

|---|---|---|

| Scoping | Undefined asset categories | Define scope in writing before any outreach |

| Wave one inquiry | Accepting incomplete responses | Set a response deadline with escalation protocol |

| Technical deep dive | Using outdated audit reports | Require audits dated within 12 months |

| Valuation | Single-source price data | Use volume-weighted average across three venues |

| Final sign-off | Verbal-only recommendations | Require written risk ratings by category |

A disciplined evaluation framework reduces avoidable risk by focusing on asset utility and structural viability rather than price momentum. That principle applies equally to a $500,000 treasury allocation and a $500 million institutional position.

Key takeaways

Effective executive digital asset due diligence requires purpose-built frameworks covering custody, valuation, regulatory exposure, and operational controls, executed in structured waves rather than a single review.

| Point | Details |

|---|---|

| Custody model is the first risk | Verify asset segregation, proof of reserves, and insurance coverage before any other assessment. |

| Valuation requires tokenomics integration | Apply modified DCF models that account for emission schedules, vesting overhangs, and liquidity discounts. |

| Regulatory mapping is non-negotiable | Document SEC classification, MiCA applicability, and jurisdictional obligations for every asset in scope. |

| Wave-based inquiry outperforms checklists | Sending questions in multiple rounds surfaces evasive responses that single-batch requests miss. |

| Process duration demands early preparation | Diligence timelines are 64% longer than a decade ago; start scoping before you think you need to. |

The governance gap most executives still underestimate

I have reviewed digital asset diligence reports from treasury teams, family offices, and institutional funds across three continents. The single most consistent failure is not technical ignorance. It is the assumption that governance structures adequate for traditional assets translate directly to digital ones.

The custody risk alone represents a category of operational exposure that has no real equivalent in equity portfolios. When a traditional custodian fails, there are regulatory backstops, SIPC protections, and legal recourse mechanisms that have been tested over decades. When a crypto custodian fails, as several have, the recovery process is a multi-year legal proceeding with uncertain outcomes and no deposit insurance. Executives who have not personally read a custody agreement, including the insurance sublimits and the force majeure clauses, are making a governance decision by omission.

The second underestimated gap is regulatory ambiguity. Most executives assume their legal team has the digital asset regulatory question covered. In practice, most corporate legal teams have generalist securities expertise and limited crypto-specific depth. The regulatory exposure assessment for a digital asset position requires counsel who has read the actual SEC enforcement actions, understands the Howey test as applied to tokens, and has tracked MiCA implementation at the member-state level. That is a narrow specialty. Finding it takes longer than most executives budget for.

My practical recommendation: treat digital asset due diligence as a standing capability, not a transaction-specific exercise. The organizations that do this well have a board-level oversight checklist that is reviewed annually, a designated digital asset risk owner, and a continuous monitoring protocol that flags material changes in custody arrangements, regulatory status, or tokenomics. The organizations that do it poorly treat it as a one-time box to check before deployment.

— Gregg

How Wush and DARE support your diligence readiness

Finance executives who want a structured, repeatable approach to digital asset governance have a practical starting point in Wush’s Digital Asset Readiness Evaluation (DARE) certification. DARE provides modular assessments across custody, compliance, legal, and operational controls, producing audit-ready documentation that maps directly to the diligence framework described in this article.

The DARE certification is designed for treasury teams, risk managers, and executives who need credentials and frameworks that regulators and counterparties recognize. It covers the governance gap that most enterprise digital asset programs leave unaddressed, from KYC/AML monitoring protocols to smart contract audit requirements. For executives who want to understand the specific advantages before committing, Wush’s edge overview outlines how the certification maps to current regulatory expectations. This is governance infrastructure, not a compliance shortcut.

FAQ

What is executive digital asset due diligence?

Executive digital asset due diligence is the structured evaluation of digital assets across custody, valuation, regulatory, and operational dimensions before investment or governance decisions. It differs from traditional due diligence because digital assets introduce non-custodial risks, tokenomics variables, and regulatory ambiguities that legacy frameworks do not address.

How long does a digital asset due diligence process take?

The due diligence process for complex transactions takes 64% longer than it did a decade ago, and digital asset reviews extend that timeline further due to technical verification requirements. Executives should budget a minimum of eight to twelve weeks for a thorough multi-stage assessment.

What are the biggest red flags in digital asset due diligence?

The most material red flags include the absence of independent smart contract audits, undocumented asset segregation practices, evasive responses across multiple inquiry waves, and legal counsel without demonstrable crypto-specific expertise. Any single one of these warrants a pause in the process.

Which custody model is safest for institutional digital asset holdings?

Institutional third-party custodians like Coinbase Custody are the gold standard for enterprise holdings because they provide proof-of-reserves reporting, segregated client assets, and insurance coverage. Exchange custody is the highest-risk option and is generally unsuitable for significant institutional positions.

How does tokenomics affect digital asset valuation?

Tokenomics directly affects fair value through emission schedules that dilute future cash flows, vesting overhangs that suppress price, and burn mechanisms that reduce supply. Valuation specialists integrate ASC 820 and IFRS 13 with blockchain analytics and tokenomics data to produce defensible figures that withstand regulatory scrutiny.