Digital Asset Insurance Coverage Evaluation Guide

Digital asset insurance coverage evaluation is the process of analyzing insurance policies to determine whether they adequately protect an institution’s cryptocurrency and digital asset holdings against specific, documented risks. Finance and risk management professionals who skip this analysis often discover coverage gaps only after a loss event. The standard industry term for this discipline is “digital asset risk transfer assessment,” though practitioners commonly call it coverage evaluation. Regulatory pressure from bodies like the SEC, combined with the growing complexity of custody arrangements, makes systematic evaluation non-negotiable. Premiums typically range from 1% to 3% of coverage amounts annually, and that cost alone justifies knowing exactly what you are buying.

What are the core components of digital asset insurance policies?

Digital asset insurance is not a single product. It is a stack of specialized policy types, each covering a distinct risk category.

The five policy types most relevant to institutional operations are custody insurance, crime insurance, directors and officers (D&O) liability, errors and omissions (E&O), and cyber insurance. Custody insurance protects assets held by a qualified custodian. Crime insurance covers employee fraud, external hacks, and extortion, but commonly excludes smart contract vulnerabilities, protocol exploits, and user errors. D&O and E&O policies address leadership decisions and professional service failures. Cyber insurance covers data breaches and system intrusions, though its overlap with crime policies creates gaps that require careful mapping.

The most consequential structural detail in any custody policy is the hot wallet sublimit. Hot wallet sublimits typically range from 2% to 5% of total assets under custody (AUC). That ceiling reflects insurer caution about internet-connected storage, and it means a custodian holding $500 million in AUC may only cover $10–25 million in hot wallet losses.

Policy structures also differ by trigger type. Occurrence-based policies cover events that happen during the policy period, regardless of when the claim is filed. Claims-made policies only respond if both the event and the claim fall within the active period. For digital assets, where breach discovery can lag months behind the incident, occurrence-based coverage is materially stronger.

| Coverage type | Typical inclusions | Common exclusions |

|---|---|---|

| Custody insurance | Cold storage theft, physical loss | Hot wallet losses above sublimit, in-transit transfers |

| Crime insurance | Employee fraud, external hacks, extortion | Smart contract exploits, protocol failures, user error |

| Cyber insurance | Data breaches, system intrusion | Social engineering, insider threats (varies by policy) |

| D&O liability | Leadership decision claims | Criminal acts, intentional misconduct |

| E&O liability | Professional service errors | Contractual penalties, known prior acts |

Pro Tip: Request the full policy schedule, not just the summary sheet. Marketing materials routinely describe coverage in broader terms than the actual policy language supports.

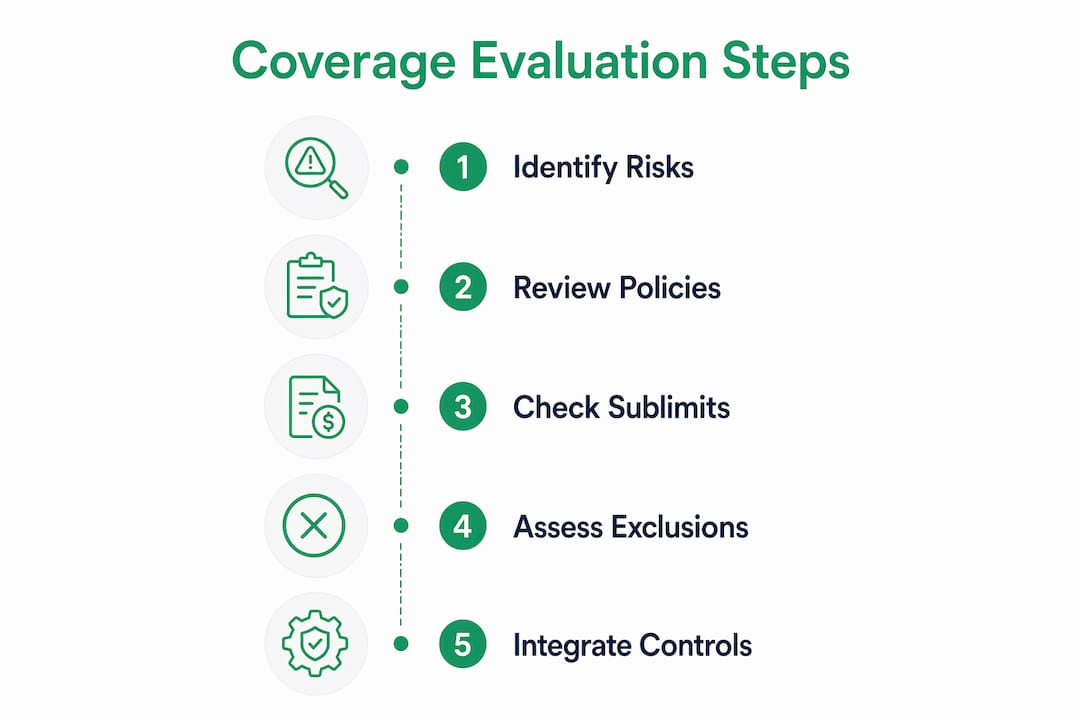

How to assess coverage adequacy against your digital asset risk exposure

Coverage adequacy assessment starts with one number: your total assets under custody. Every other calculation flows from it.

Follow these steps to map your risk exposure to your policy terms:

- Calculate your hot wallet exposure. Identify what percentage of AUC sits in internet-connected wallets at any given time. Compare that figure to the policy’s hot wallet sublimit. If your operational hot wallet balance regularly exceeds the sublimit, you have an uninsured gap.

- Audit in-transit transfer coverage. Many custody policies exclude assets during the transfer process. Map every transfer workflow and confirm whether the policy covers assets in transit between wallets, exchanges, or counterparties.

- Verify named insured status. Most digital asset policies name the custodian or exchange as the insured party, not the client. Clients are beneficiaries only to the extent of the custodian’s coverage. Confirm your institution’s standing in the policy hierarchy before assuming protection.

- Analyze aggregate limits versus per-client limits. Headline insurance limits often represent aggregate maximums shared across all clients, not per-client guarantees. A $200 million aggregate limit shared across 50 institutional clients provides far less protection than it appears.

- Identify protocol and technology risk gaps. Standard policies rarely cover losses from smart contract failures, oracle manipulation, or governance attacks. If your institution holds DeFi positions or staked assets, those exposures are almost certainly uninsured.

- Map deductibles to your loss tolerance. High deductibles reduce premiums but shift meaningful risk back to the institution. Confirm that your deductible level aligns with your board-approved risk appetite.

Understanding digital asset exposure limits in practical terms helps finance teams translate abstract policy numbers into operational decisions. The goal is not to find a policy with the largest headline number. The goal is to find a policy whose actual scope matches your actual risk profile.

Pro Tip: Ask your custodian for a certificate of insurance that names your institution as an additional insured or loss payee. Without that documentation, your coverage claim in a dispute is significantly weaker.

Which common exclusions should risk managers watch out for?

Policy exclusions are where coverage evaluation becomes most consequential. The exclusions that appear most frequently across digital asset policies include:

- User error and operational mistakes. Sending assets to an incorrect address, misconfiguring a wallet, or approving a fraudulent transaction typically falls outside coverage. This is one of the most common loss events in practice.

- Social engineering and phishing. Attackers who manipulate employees into authorizing transfers are rarely covered under standard crime policies. Some insurers offer social engineering endorsements, but they carry their own sublimits.

- Smart contract and protocol failures. Losses from smart contract exploits and protocol-level vulnerabilities are excluded from most policies. This gap is material for any institution with DeFi or tokenized asset exposure.

- Market price declines. No standard policy covers losses from asset devaluation. This seems obvious, but institutions sometimes conflate market risk with insurable risk during coverage reviews.

- Valuation disputes. Valuation of lost digital assets is commonly disputed. Payout basis can be the time of loss, the time of discovery, or a capped maximum at insurer discretion. Without a clear valuation clause, a claim settlement can fall far below the actual loss.

The valuation issue deserves special attention. Bitcoin’s price can move 20% in 48 hours. A policy that values a loss at the time of discovery rather than the time of incident can produce a dramatically different payout. Negotiating a specific valuation methodology into the policy language is one of the highest-value steps in any coverage evaluation.

Pro Tip: Push for a valuation clause that specifies the price source (such as a named exchange index), the time of measurement, and the currency of settlement. Ambiguity here benefits the insurer, not you.

How to incorporate insurance evaluation into your risk management framework

Insurance is a last resort, not a primary control. Large headline coverage figures often mask limited scopes that exclude in-transit transfers and hot wallet risks. Treating insurance as your primary defense against digital asset loss is a governance failure.

The correct model places operational controls first. Multi-signature authorization, cold storage protocols, security audits, and access controls reduce the probability of loss. Insurance responds to residual risk that controls cannot eliminate. This hierarchy matters because insurers themselves require evidence of strong controls before underwriting meaningful coverage. Weak controls produce either rejected applications or prohibitively high premiums.

Build insurance evaluation into your vendor selection process. When assessing a custodian, request their full insurance documentation as part of due diligence. Evaluate the custodian’s coverage as you would any other operational control: by scope, by limit, and by the conditions under which it responds. Monitoring digital asset market risk continuously also informs when coverage limits need to be renegotiated, particularly during periods of rapid asset appreciation.

Annual policy renewal is the most underused opportunity in institutional risk management. Standardized custody insurance premiums decreased approximately 40% year-over-year as of april 2026, driven by improved security practices and market competition. That pricing shift creates real negotiating leverage. Risk managers who renew passively leave both coverage improvements and cost reductions on the table.

Integrate coverage review into your broader risk appetite statement. Set explicit thresholds: if AUC grows beyond a defined level, trigger a policy review. If a new asset class is added to the portfolio, require a coverage gap analysis before onboarding. This turns insurance evaluation from a reactive exercise into a proactive governance practice. Understanding institutional custody arrangements is foundational to this process, since coverage scope is directly tied to how assets are held.

Key Takeaways

Effective digital asset insurance coverage evaluation requires matching policy scope, sublimits, and exclusions to your institution’s actual risk profile, not its headline coverage figure.

| Point | Details |

|---|---|

| Hot wallet sublimits are binding | Sublimits of 2%–5% of AUC cap coverage where losses are most likely to occur. |

| Aggregate limits dilute per-client protection | Shared policy limits across clients can leave individual institutions severely underinsured after a major breach. |

| Exclusions define real coverage | User error, social engineering, and smart contract failures are excluded from most standard policies. |

| Valuation clauses determine payouts | Negotiate specific price sources and timing into the policy to avoid post-loss disputes. |

| Insurance follows controls, not replaces them | Strong operational controls are a prerequisite for meaningful coverage, not an alternative to it. |

The detail that separates adequate coverage from a false sense of security

The most common mistake I see finance teams make is treating the policy limit as the measure of protection. A custodian advertising $500 million in coverage sounds reassuring. But if that limit is aggregate across dozens of clients, excludes hot wallet losses above 3% of AUC, and values claims at the time of discovery rather than the time of loss, the actual protection for your institution may be a fraction of what you assumed.

The Bitcoin market risk profile makes valuation timing especially consequential. Price volatility means the gap between loss-time and discovery-time valuation can be enormous. I have seen institutions assume they were fully covered, only to find that the combination of sublimits, aggregate sharing, and valuation methodology reduced their effective recovery to less than 20% of actual loss.

My advice is to read the exclusions section before the coverage section. The exclusions tell you what the policy actually does. The coverage section tells you what it might do under ideal conditions. Real risk management lives in the gap between those two descriptions. Wush’s DARE framework addresses this gap directly by building policy scrutiny into the governance assessment process, rather than treating insurance as a checkbox.

— Gregg

Wush DARE: structured evaluation for digital asset coverage gaps

Finance and risk management professionals who want a systematic approach to coverage evaluation have a structured option in Wush’s Digital Asset Readiness Evaluation (DARE). The DARE certification program covers custody governance, regulatory compliance, and risk management controls, including the insurance evaluation criteria that most internal frameworks overlook.

DARE’s modular assessment process helps teams identify specific coverage gaps, benchmark custodian insurance documentation against institutional standards, and build a defensible compliance record. The program includes annual renewal to keep pace with market changes, including the premium compression and coverage evolution that characterized 2026. For institutions that need credentials to demonstrate governance maturity to boards or regulators, the DARE certification provides a recognized, blockchain-supported credential that documents the evaluation process itself.

FAQ

What is digital asset insurance coverage evaluation?

Digital asset insurance coverage evaluation is the systematic analysis of insurance policies to confirm they adequately cover an institution’s specific cryptocurrency and digital asset risks. It examines policy scope, sublimits, exclusions, and valuation methods against actual risk exposure.

What are hot wallet sublimits and why do they matter?

Hot wallet sublimits cap coverage for internet-connected storage, typically at 2%–5% of total assets under custody. They matter because hot wallets carry the highest operational risk and are where most theft events occur.

Are clients directly covered by a custodian’s insurance policy?

Most digital asset policies name the custodian as the insured party. Clients are beneficiaries only to the extent of the custodian’s coverage, which means named insured status and aggregate limit structure directly affect client recovery in a loss event.

What exclusions most commonly undermine digital asset coverage?

User error, social engineering, phishing, and smart contract protocol failures are excluded from most standard policies. These categories represent a significant share of actual digital asset loss events, making them the most consequential gaps in typical coverage.

How often should institutions review their digital asset insurance policies?

Institutions should review coverage at every annual renewal, after any significant change in assets under custody, and whenever a new asset class or custodian is added. Premium decreases in 2026 create additional incentive to renegotiate terms proactively rather than accept automatic renewals.