Digital Asset Identity Verification Explained for Professionals

Digital asset identity verification is defined as the process of confirming ownership and control of digital assets using cryptographic proofs, decentralized identifiers (DIDs), and regulatory-compliant credential frameworks. This is not a simple username check. It combines on-chain registries, verifiable credentials, and standards like FATF Recommendation 16 to confirm who controls what, and whether that control is legitimate. For finance teams, risk managers, and compliance officers, understanding this process is no longer optional. The stakes include regulatory penalties, custody failures, and breach exposure from outdated centralized identity models.

What is digital asset identity verification?

Digital asset identity verification is the technical and regulatory process of validating that a person or entity genuinely controls a digital asset, using cryptographic evidence rather than self-reported claims. The industry term for the broader discipline is decentralized identity, which encompasses DIDs, verifiable credentials (VCs), and zero-knowledge proofs (ZKPs). These tools work together to confirm identity without exposing raw personal data to third parties.

Two distinct layers define the process. The first is authentication: proving that a user controls a private key linked to a wallet address. The second is compliance: confirming that the verified identity meets regulatory requirements, such as sanctions screening or anti-money laundering (AML) checks under FATF guidelines. Both layers must function together for an organization to operate safely in the digital asset space.

The gap between these two layers is where most organizations run into trouble. A user can authenticate a wallet without ever passing a compliance check. Conversely, a compliance check can be completed without confirming actual on-chain control. Effective digital asset verification closes both gaps simultaneously.

How does blockchain enable secure identity verification?

Blockchain enables secure identity verification by recording cryptographic proofs on an immutable ledger, making it possible to confirm wallet ownership and credential validity without relying on a central authority. A digital wallet’s private key serves as the primary proof of ownership. When a user signs a transaction or a challenge message with that key, the signature confirms control without revealing the key itself.

On-chain identity registries extend this further. The Cross-Chain Identity (CCID) model allows a single verification event to issue a reusable credential linked to multiple blockchain addresses. This eliminates the need for repeated KYC checks every time a user interacts with a new protocol or chain. One verified identity maps to several wallet addresses across different blockchains, persisting compliance status across environments.

Pro Tip: Confirm that your identity registry supports multiple wallet addresses per user before deployment. Registries that map only one address per identity force users to re-verify on every new chain, creating friction and compliance gaps.

Reusable KYC compounds this benefit. Reusable credentials issued once can be instantly accepted by multiple regulated entities, allowing a user verified on one platform to onboard to another without uploading documents again. This reduces onboarding time from days to seconds for returning users. For treasury teams managing positions across multiple protocols, this is a material operational improvement.

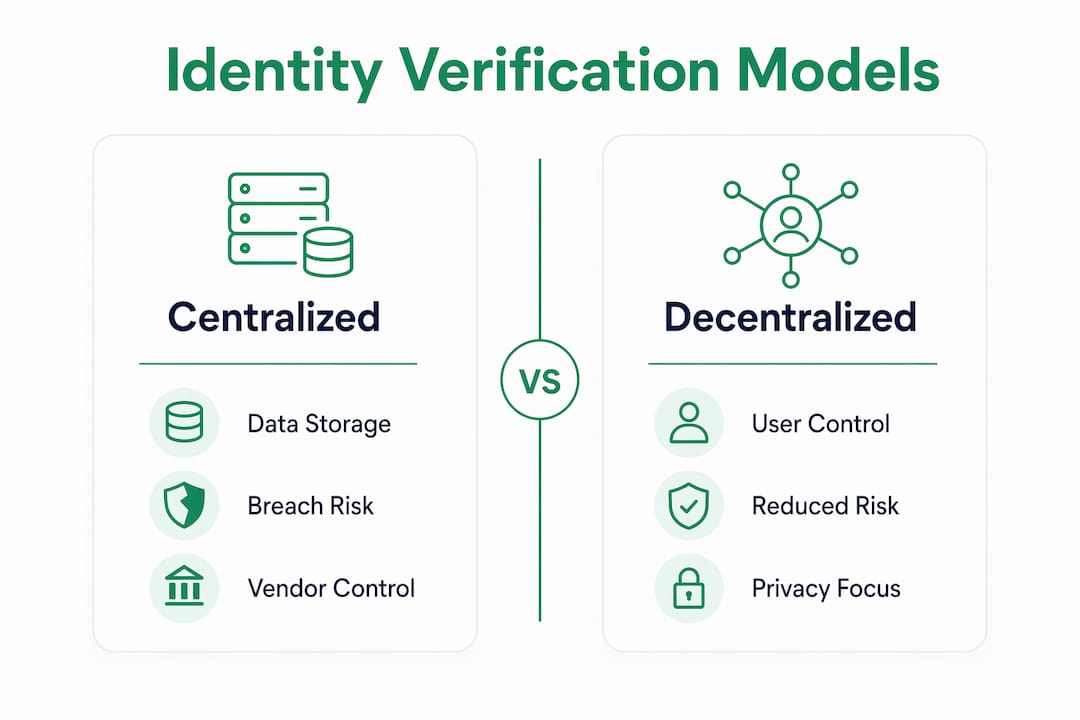

Centralized vs. decentralized identity architectures

The difference between these two models is not just technical. It is a risk management decision.

Centralized identity systems store personal data in a vendor’s database. Every breach of that database exposes user PII directly. Decentralized systems store credentials in the user’s own wallet. The vendor never holds the raw data, so a breach of the vendor’s infrastructure does not compromise user identity. Firms relying on centralized PII storage increase their cybersecurity breach surface significantly. Shifting to decentralized models moves compliance audit trails to privacy-preserving mechanisms instead.

What is the difference between provenance and ownership?

Provenance and ownership are distinct concepts, and conflating them is one of the most common compliance errors in digital asset management. Digital asset verification involves two key elements: provenance, which traces an asset’s origin and transaction history, and ownership, which confirms current control through private key access.

Provenance answers the question: where has this asset been? It covers the chain of custody from minting or first issuance through every subsequent transfer. Ownership answers a different question: who controls this asset right now? A marketplace interface may display a wallet’s holdings, but that display does not constitute proof of ownership. Cryptographic signature challenges confirm true ownership. API checks and marketplace status can be spoofed.

Pro Tip: Never accept a screenshot or marketplace display as proof of ownership in a compliance context. Always require a signed message from the wallet address in question, verified against the on-chain public key.

Verification methods differ by purpose:

- Provenance verification: on-chain transaction history review, block explorer analysis, NFT or token minting records, and transfer event logs

- Ownership verification: cryptographic signature challenges, wallet connection with message signing, and private key proof via hardware wallet attestation

Compliance officers need both. Provenance without ownership confirmation leaves open the possibility that the asset was transferred after the history check. Ownership without provenance leaves open questions about the asset’s origin and whether it passed through sanctioned addresses.

How do verifiable credentials improve privacy and security?

Verifiable credentials improve privacy by allowing users to prove facts about themselves without revealing the underlying documents. Decentralized KYC issues users verifiable credentials held in their own wallets. When a regulated platform requests verification, the user presents a zero-knowledge proof derived from that credential. The proof confirms the relevant fact, such as age, nationality, or sanctions status, without transmitting the passport scan or personal data behind it.

This model aligns with internationally recognized standards. Verifiable credentials and decentralized identity meet the W3C VC Data Model 2.0 specification and comply with FATF virtual asset guidelines. Compliance frameworks increasingly recognize verifiable credentials as suitable for AML checks, sanctions screening, and customer due diligence. That recognition matters for organizations that need to demonstrate regulatory alignment to auditors and regulators.

The practical benefits of this model are significant:

- No central PII database: credentials live with the user, not the vendor, removing the most common breach target

- Instant re-verification: a credential issued once works across multiple platforms without document re-submission

- Selective disclosure: users share only the specific attributes required, not their full identity record

- Audit trail integrity: cryptographic proofs create tamper-evident records suitable for regulatory review

Pro Tip: When transitioning from a centralized identity model, start by issuing verifiable credentials for new users while maintaining legacy records for existing ones. A phased migration reduces operational risk and gives your compliance team time to validate the new workflow.

For organizations managing self-sovereign identity models, the reduction in breach surface is the most immediate security gain. Removing PII from vendor infrastructure does not eliminate compliance obligations. It shifts where those obligations are fulfilled, from a central database to a cryptographically secured credential in the user’s control.

What regulatory frameworks govern digital asset identity verification?

FATF Recommendation 16, commonly called the Travel Rule, is the primary regulatory framework shaping identity verification for digital assets. It requires Virtual Asset Service Providers (VASPs) to collect and transmit originator and beneficiary identity data for transactions above defined thresholds. The data must travel with the transaction, similar to how wire transfer regulations work in traditional banking.

The compliance challenge is transmitting this data without exposing PII to unauthorized parties. Structured, verifiable credential formats solve this. Rather than sending a raw data file with personal details, a VASP can transmit a cryptographic proof that the required identity data exists and has been verified, without revealing the data itself. Verification on some identity-as-a-service platforms takes as little as 2 seconds for returning users. That speed matters when transaction throughput is high and manual review creates bottlenecks.

Implementing compliance-ready digital asset verification requires a structured approach:

- Map your transaction flows. Identify every point where originator or beneficiary identity data must be collected or transmitted under FATF Recommendation 16.

- Select a credential format. Choose a verifiable credential standard, such as W3C VC Data Model 2.0, that your counterparty VASPs can accept and verify.

- Integrate on-chain identity registries. Connect wallet addresses to verified credentials so that compliance status is readable at the protocol level.

- Implement ZKP-based disclosure. Configure your system to share only the attributes required by the receiving VASP, not the full identity record.

- Establish renewal and revocation processes. Credentials must be revocable if a user’s status changes, such as a new sanctions listing, and renewed on a defined schedule.

The regulatory risk implications of non-compliance extend beyond fines. VASPs that cannot demonstrate Travel Rule compliance face delistings, correspondent banking restrictions, and reputational damage that is difficult to reverse. Building the technical infrastructure now, before enforcement intensifies, is the lower-cost path.

Key Takeaways

Digital asset identity verification requires cryptographic ownership proof, regulatory-compliant credential frameworks, and a clear separation between provenance tracking and current ownership confirmation.

| Point | Details |

|---|---|

| Ownership requires cryptographic proof | Marketplace displays do not confirm ownership; signed wallet challenges do. |

| Provenance and ownership are separate checks | Compliance requires both asset history and current control verification. |

| Decentralized credentials reduce breach risk | Storing credentials in user wallets removes PII from vendor databases. |

| FATF Recommendation 16 drives VASP obligations | VASPs must transmit identity data with transactions above defined thresholds. |

| Reusable KYC cuts onboarding friction | One verified credential works across multiple platforms without re-submission. |

Why identity verification must be treated as a lifecycle, not a checkpoint

The most persistent mistake I see organizations make is treating identity verification as a one-time event. A user passes KYC at onboarding, gets a green light, and the file closes. Six months later, that same user appears on a new sanctions list, or their wallet address is linked to a flagged transaction. The original verification is now worthless, and the organization has no mechanism to detect the change.

Identity verification is a continuous lifecycle process. Decentralized identity makes ongoing proof practical because credentials can be revoked and reissued without requiring the user to restart the full onboarding process. That is a structural advantage over centralized models, where updating a user’s status requires touching a central database that is itself a breach target.

The second mistake I see regularly is failing to separate provenance from ownership in the verification workflow. Teams assume that because they can see an asset in a wallet on a block explorer, they have confirmed ownership. They have not. They have confirmed that the asset is associated with an address. Confirming that the person in front of them controls that address requires a signature challenge. Skipping that step is a compliance gap that auditors will find.

My recommendation for organizations planning to adopt these methods is to start with the governance credentials framework before selecting technology. The technology choices follow from the governance model, not the other way around. Organizations that reverse this order end up with tools that do not fit their compliance obligations.

— Gregg

How Wush’s DARE certification supports your verification readiness

Knowing the theory of digital asset identity verification is one thing. Knowing whether your organization’s current processes actually meet the standard is another question entirely.

Wush’s Digital Asset Readiness Evaluation (DARE) is a structured certification program that helps finance teams, risk managers, and compliance officers assess exactly where their identity verification and governance processes stand. The DARE certification covers custody controls, regulatory compliance, and operational risk across the full digital asset lifecycle. It identifies gaps before regulators or auditors do, and it provides a credential that demonstrates verified readiness to counterparties and stakeholders. Annual renewal keeps your certification current as regulatory standards evolve. For organizations serious about operating in the digital asset space with confidence, DARE is the structured starting point.

FAQ

What is digital asset identity verification?

Digital asset identity verification is the process of confirming that a person or entity genuinely controls a digital asset using cryptographic proofs, verifiable credentials, and regulatory-compliant identity frameworks. It combines on-chain ownership confirmation with compliance checks such as AML screening and sanctions verification.

How does a zero-knowledge proof work in identity verification?

A zero-knowledge proof allows a user to prove a specific fact, such as passing a sanctions check, without revealing the underlying personal data. The verifier receives cryptographic confirmation that the fact is true, not the documents or data behind it.

What is FATF Recommendation 16 and why does it matter?

FATF Recommendation 16, known as the Travel Rule, requires VASPs to collect and transmit originator and beneficiary identity data for transactions above defined thresholds. Non-compliance can result in regulatory penalties, delistings, and loss of correspondent banking access.

What is the difference between provenance and ownership in digital assets?

Provenance traces an asset’s full transaction history from origin to present. Ownership confirms that a specific person currently controls the asset through private key access. Both are required for complete compliance verification, and neither substitutes for the other.

What is a reusable KYC credential?

A reusable KYC credential is a verifiable credential issued after a single identity verification event that can be accepted by multiple regulated platforms without requiring the user to submit documents again. It reduces onboarding time and eliminates redundant verification across protocols.