The Role of C-Suite in Digital Asset Compliance

The C-suite’s role in digital asset compliance is defined as the direct legal, fiduciary, and operational accountability executives hold for their organization’s adherence to digital asset regulations. This is not a delegated function. Under frameworks like MiCA, DORA, and NIS2, regulators hold senior leadership personally responsible for governance failures. As of 2026, that personal exposure now includes civil, administrative, and criminal penalties. Executives who treat compliance as a back-office task are misreading both the regulatory environment and their own legal position. The standard industry term for this accountability structure is “digital asset governance,” and it sits squarely at the board level.

What are the key regulatory frameworks shaping C-suite responsibilities?

Three regulations define the current executive compliance landscape: MiCA, DORA, and NIS2. Each one places explicit obligations on management bodies, not just compliance teams.

MiCA requires that Crypto Asset Service Providers’ management bodies collectively possess the skills and experience to oversee regulatory compliance. That language is deliberate. Regulators are not satisfied with a single designated compliance officer. The entire board must demonstrate competence. MiCA also mandates independent compliance and risk functions, documented risk management frameworks, and annual independent audits of AML/CFT controls with strict separation from commercial operations.

NIS2 and DORA impose legal accountability and potential personal penalties on management bodies for cybersecurity risk management failures. Executives face civil, administrative, and criminal exposure under these laws. That is a material shift from prior regulatory regimes, where enforcement typically targeted the firm rather than the individual.

Regulators audit executive decisions and board oversight rather than titles or slogans. Board minutes and governance artifacts are reviewed to verify leadership engagement and compliance maturity.

The practical implication is clear. Boards must approve key risk policies, document their deliberations, and demonstrate active oversight. A board that rubber-stamps management recommendations without substantive review is a regulatory liability. Executives who want to understand the full scope of their board-level oversight duties should treat these three frameworks as the baseline, not the ceiling.

How should C-suite executives architect governance frameworks?

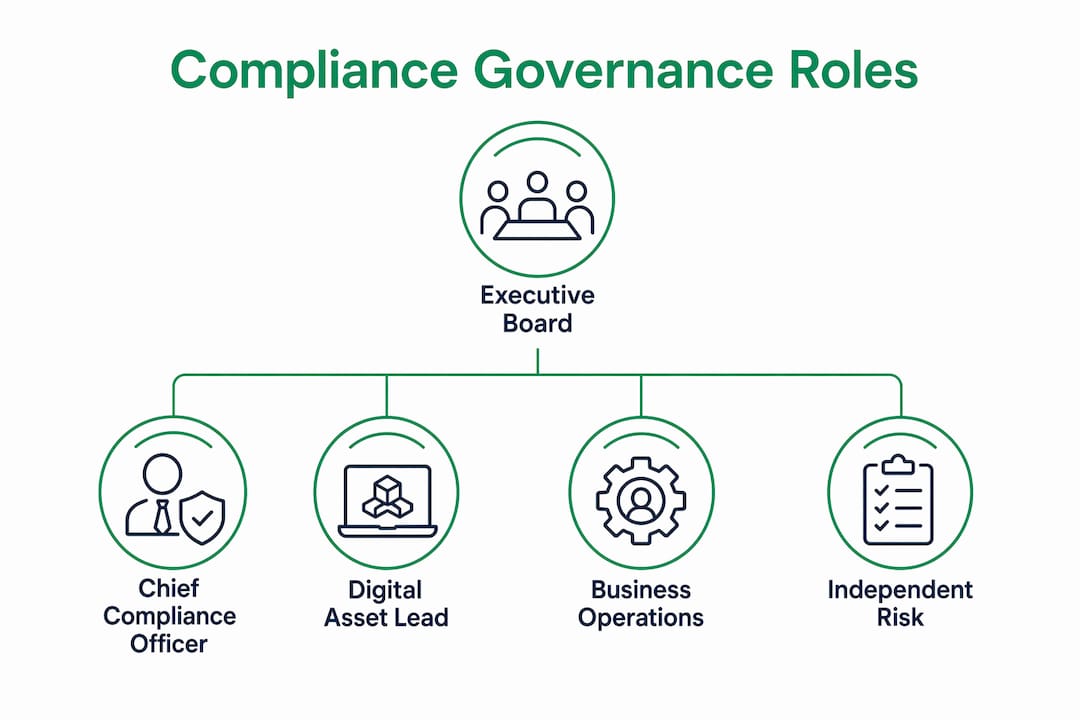

The three-lines-of-defense model is the accepted structure for digital asset governance. The first line is business operations, the second is independent risk and compliance functions, and the third is internal audit. Each line must be genuinely independent from the others.

Overconcentration of compliance responsibilities in too few senior roles is flagged as a governance weakness by regulators. This is a common failure pattern in firms new to digital assets. A CFO who also chairs the risk committee while supervising the compliance officer creates a structural conflict that regulators will identify and penalize.

The table below maps the primary governance roles to their compliance responsibilities:

| Role | Primary compliance responsibility |

|---|---|

| Chief Compliance Officer (CCO) | Owns the compliance program, monitors red flags, escalates material issues |

| Chief Financial Officer (CFO) | Oversees financial controls, AML/CFT reporting, and treasury risk |

| Chief Technology Officer (CTO) | Manages cybersecurity controls, DORA readiness, and system resilience |

| Chief Risk Officer (CRO) | Maintains the risk framework, second-line independence, and board reporting |

| Board Risk Committee | Reviews management reporting, approves risk appetite, and documents decisions |

Appointing a dedicated digital asset compliance lead, separate from the general CCO function, is a governance upgrade that regulators view favorably. This person should have direct access to the board risk committee without routing through commercial leadership. That direct line is not a formality. It is the mechanism that keeps the second line genuinely independent.

Pro Tip: Document every board decision on digital asset risk in meeting minutes with enough specificity to show regulators that leadership engaged with the substance of the issue, not just the summary.

Digital asset risk management is now commonly placed under the Chief Compliance Officer or Head of Financial Crime, with direct reporting lines to board risk committees as the standard as of Q2 2026. That reporting structure is not optional under MiCA or DORA. It is a design requirement.

What practical steps can C-suite take to embed compliance in operations?

Compliance embedded in daily operations outperforms compliance reviewed quarterly. The difference is not philosophical. It is the difference between catching a problem before it becomes a regulatory event and discovering it during an audit.

Compliance must be embedded and proactive, with the CCO functioning as an active operating control rather than a post-facto auditor. That means the CCO participates in product decisions, new asset onboarding reviews, and counterparty assessments in real time, not after the fact. Executives should build this expectation into the CCO’s mandate explicitly.

The following steps translate that principle into operational practice:

- Establish a compliance reporting cadence. The CCO should report to the board risk committee on a fixed schedule, at minimum quarterly, with a defined set of risk metrics, open findings, and escalation items.

- Define red flag escalation protocols. Effective CCOs design monitoring systems that distinguish isolated incidents from systemic risks and escalate concerns to the board before they become enforcement matters.

- Separate second-line functions from commercial pressure. Compliance officers must not report to revenue-generating business heads. That structural independence is a MiCA requirement and a basic governance standard.

- Maintain audit readiness continuously. Regulators do not announce visits. Firms that treat audit preparation as a periodic exercise rather than a permanent state consistently underperform in regulatory reviews.

- Review your AML/CFT program annually with an independent auditor. The independent AML/CFT audit requirement under MiCA is not satisfied by an internal review. The auditor must be independent from the compliance function being assessed.

Boards must avoid day-to-day operational execution but require regular, comprehensive reporting on digital asset risks and compliance findings to fulfill their fiduciary obligations. That balance, oversight without micromanagement, is the governance posture regulators expect. For a detailed breakdown of what that reporting should cover, the AML compliance checklist published by Wush provides a practical reference point.

How do fiduciary duties and personal liability affect executive decisions?

Personal liability is the sharpest edge of the 2026 regulatory environment. Executives who assumed that corporate structure insulated them from individual enforcement actions are now reading enforcement notices addressed to them by name.

Regulators review board meeting minutes and governance artifacts to assess leadership engagement and compliance maturity. A board that cannot produce documented evidence of substantive compliance oversight is a board that cannot defend itself in an enforcement proceeding. The documentation is not bureaucracy. It is your legal defense.

The personal liability risks executives face in 2026 include:

- Administrative fines imposed directly on individual board members for governance failures under NIS2 and DORA.

- Temporary or permanent bans from holding management positions in regulated entities.

- Criminal referrals in cases involving willful disregard of AML/CFT obligations.

- Reputational damage that follows enforcement actions regardless of the legal outcome.

Boards should require regular, comprehensive management reporting on digital asset performance, risk, and audit findings. That reporting serves a dual purpose. It keeps the board informed, and it creates the documented record that demonstrates active oversight. Both functions matter equally.

Pro Tip: Retain external legal counsel with digital asset regulatory experience to review your governance documentation annually. The cost of that review is a fraction of the cost of a single enforcement action.

The legal risk management guide from Wush covers the specific documentation practices that protect executives from administrative and criminal exposure under current frameworks.

Key takeaways

The C-suite’s role in digital asset compliance is a direct legal obligation under MiCA, DORA, and NIS2, requiring documented governance, independent compliance functions, and personal accountability at the board level.

| Point | Details |

|---|---|

| Personal liability is real | NIS2 and DORA expose individual executives to fines, bans, and criminal referrals. |

| Documentation is your defense | Regulators audit board minutes to verify substantive compliance engagement. |

| Three-lines-of-defense is mandatory | Independent risk, compliance, and audit functions must be structurally separated. |

| CCO must be proactive | Compliance embedded in daily operations catches problems before they become enforcement events. |

| Board oversight is not execution | Boards set risk appetite and review reporting; they do not run compliance programs. |

Why compliance leadership is harder than it looks

The executives I see struggle most with digital asset governance are not the ones who ignore compliance. They are the ones who delegate it completely and assume the problem is solved. That is the most dangerous posture in the current regulatory environment.

“Tone at the top” has become a concrete statutory duty. Regulators are no longer satisfied with a compliance policy document and a designated officer. They want to see evidence that the board engaged with the substance of compliance decisions, challenged management assumptions, and documented its reasoning. That requires a different kind of executive involvement than most boards are accustomed to.

The firms that get this right share one characteristic: their CCO has genuine authority and direct board access. Not a dotted-line relationship to the board through the CEO. A direct line. When the CCO identifies a material risk, the board hears about it before the commercial team has a chance to frame the narrative. That structural independence is what separates governance that works from governance that looks good on paper.

The other mistake I see repeatedly is treating compliance as a cost center to be minimized. Under MiCA and DORA, under-resourcing your compliance function is not a budget decision. It is a governance failure that regulators will identify and penalize. The firms investing in compliance infrastructure now are buying insurance against enforcement actions that cost orders of magnitude more.

— Gregg

How DARE helps executives benchmark compliance readiness

Knowing your obligations is the first step. Knowing whether your organization actually meets them is harder.

Wush built the DARE certification specifically for this gap. The Digital Asset Readiness Evaluation gives executives a structured, independent assessment of their organization’s compliance posture across custody, AML/CFT, risk management, legal controls, and operational governance. The program aligns directly with MiCA, DORA, and NIS2 requirements, so the assessment reflects what regulators actually look for. Annual renewal keeps your certification current as the regulatory environment evolves. For executives who need a credible benchmark to present to their board or regulator, DARE provides the framework and the credential.

FAQ

What is the C-suite’s primary role in digital asset compliance?

The C-suite is legally accountable for setting governance frameworks, approving risk policies, and ensuring independent compliance functions operate effectively. Under MiCA, DORA, and NIS2, this accountability extends to personal liability for individual executives.

Which regulations impose personal liability on executives for digital asset failures?

NIS2 and DORA both impose civil, administrative, and criminal exposure on management bodies for cybersecurity and operational risk failures. MiCA adds governance requirements specific to crypto asset service providers.

How often should the board receive compliance reporting on digital assets?

Boards should receive comprehensive compliance reporting at minimum quarterly, covering risk metrics, open audit findings, and any material escalations from the CCO or Chief Risk Officer.

What is the three-lines-of-defense model in digital asset governance?

The three-lines-of-defense model separates business operations (first line), independent risk and compliance functions (second line), and internal audit (third line). Each line must be structurally independent to meet regulatory expectations under MiCA and DORA.

How can executives protect themselves from personal enforcement actions?

Executives protect themselves by documenting board deliberations thoroughly, maintaining structurally independent compliance functions, and retaining external legal counsel to review governance practices annually.