Risk Frameworks in Digital Finance: 2026 Guide

Risk frameworks in digital finance are defined as structured methodologies that identify, assess, mitigate, and monitor risks across digital financial operations, from payments infrastructure to crypto asset custody. The role of risk frameworks in digital finance has never been more consequential. Global data breaches in 2025 averaged $4.44 million per incident worldwide, with U.S. costs reaching $10.22 million. That number alone explains why governance professionals are treating frameworks like COSO ERM, ISO 31000, and the NIST Risk Management Framework not as compliance paperwork, but as operational infrastructure. Add DORA’s EU-wide mandate and the rapid spread of AI-driven financial services, and the pressure to build credible, auditable risk governance has become a board-level priority.

What is the role of risk frameworks in digital finance?

Risk frameworks in digital finance serve three functions: they create a common language for risk across the organization, they produce documented evidence that regulators can audit, and they connect enterprise strategy to operational controls. Without a framework, risk management defaults to individual judgment, which is inconsistent and unscalable.

The core elements of any credible framework follow a consistent pattern. Risk identification maps exposures across business lines. Assessment scores those exposures by likelihood and impact. Mitigation defines controls, owners, and timelines. Monitoring tracks control effectiveness over time. This cycle is not a one-time exercise. Risk frameworks must be dynamic, explicitly referenced in board reports and third-party audits rather than filed away after implementation.

DORA, which applied across the EU from january 2025, illustrates how regulatory pressure accelerates framework adoption. The regulation mandates ICT third-party contract registers and a unified approach to incident reporting, forcing banks and fintechs to formalize what many had previously managed informally. Regulatory risk in digital assets now demands the same rigor as credit or market risk.

What are the core pillars of a digital finance risk framework?

Effective digital finance risk architecture in 2026 is built on five pillars: board oversight, defined accountability, independent risk and compliance functions, incident escalation discipline, and automated workflow monitoring. Each pillar addresses a specific governance failure mode that regulators and auditors look for.

Board oversight means the board receives structured risk reporting on a defined cadence, not just when something goes wrong. Defined accountability assigns named owners to every material risk, so escalation paths are clear before an incident occurs. Independent risk and compliance functions prevent the business line from self-certifying its own risk posture. Incident escalation discipline ensures that threshold breaches trigger documented responses within agreed timeframes. Automated workflow monitoring replaces manual sampling with continuous control testing.

Operational controls sit beneath these pillars. Multi-factor authentication, end-to-end encryption, and real-time compliance monitoring are the technical layer. They generate the data that feeds the governance layer above them. Without that data flow, board oversight is theoretical rather than evidence-based.

Pro Tip: Avoid siloed risk management by integrating financial, operational, and compliance risks into a single enterprise risk management view. Siloed risk management produces inconsistent scoring, delayed escalation, and fragmented reporting, all of which regulators treat as governance failures.

How do leading risk frameworks compare for digital finance?

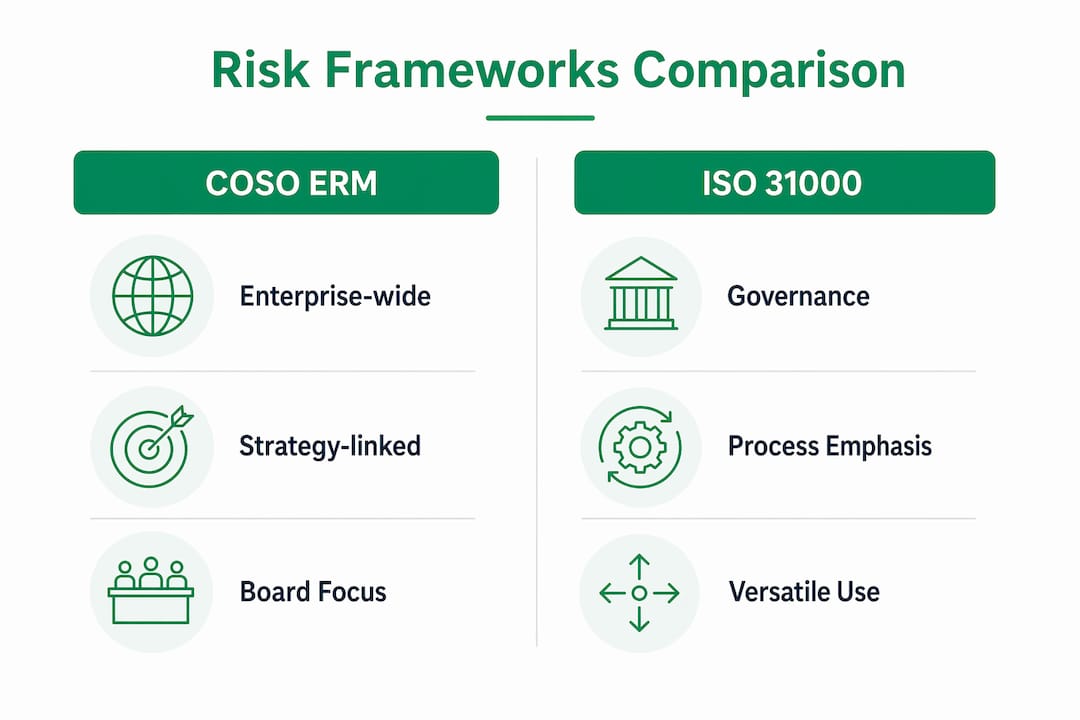

Finance professionals rarely implement a single framework in isolation. The practical reality is that COSO ERM, ISO 31000, NIST RMF, FAIR, and ISO/IEC 27005 each address different dimensions of risk, and most mature organizations layer two or more together.

| Framework | Primary Focus | Ideal Use Case | Key Strength |

|---|---|---|---|

| COSO ERM | Enterprise-wide strategic risk | Banks, asset managers, public companies | Connects risk to business objectives |

| ISO 31000 | Principles and guidelines for risk management | Any industry, including fintech | Flexible, internationally recognized |

| NIST RMF | Information security and system risk | Financial institutions with federal exposure | Detailed control catalog |

| FAIR | Quantitative financial risk analysis | Cyber risk quantification for CFOs | Translates risk into dollar terms |

| ISO/IEC 27005 | Information security risk management | Digital asset custodians, cloud-native fintechs | Aligns with ISO 27001 certification |

COSO ERM works best when the board needs risk tied directly to strategic objectives. ISO 31000 provides the governance principles that sit above all other frameworks, making it a natural starting point. NIST RMF delivers the control specificity that information security teams need. FAIR fills the gap that narrative frameworks leave open: it quantifies cyber risk in financial terms, which CFOs and audit committees can act on directly.

For digital finance contexts specifically, crypto asset platforms and AI-driven lending models require adaptation beyond what any single framework covers out of the box. Digital assets require new risk models because programmatic risks in blockchain environments demand automated cryptographic verification rather than traditional human-dependent controls. Layering NIST RMF controls onto a COSO ERM governance structure, with ISO 31000 principles as the connective tissue, is the approach most compliance teams are converging on in 2026.

How do finance professionals implement risk frameworks in practice?

Implementation follows five stages, and skipping any one of them produces a framework that looks complete on paper but fails under regulatory scrutiny.

- Assessment. Map your current risk exposures across financial, operational, and compliance dimensions. Use a digital financial risk assessment template that captures both quantitative scores and qualitative context. Document gaps between current controls and framework requirements.

- Design. Select the framework or framework combination appropriate to your regulatory environment and business model. Define governance structures, escalation thresholds, and reporting cadences. Assign named risk owners at every level.

- Implementation. Deploy controls, configure automated monitoring tools, and train staff on escalation protocols. For EU-regulated entities, this stage must address DORA’s ICT third-party requirements directly.

- Monitoring. Run continuous control testing rather than periodic sampling. AI-driven monitoring tools now detect anomalies in transaction patterns and access logs in real time, which reduces the window between control failure and detection.

- Review. Conduct formal framework reviews at least annually, or after any material incident or regulatory change. Third-party audits add credibility to internal assessments. Strategic risk management frameworks require governance calendars and audit trail management to satisfy oversight requirements.

EU banks integrating DORA compliance into existing risk frameworks found that the most time-consuming step was building the ICT third-party contract register. Many had vendor relationships documented across multiple systems with no single owner. That discovery alone justified the implementation effort. For a practical governance checklist, the board-level oversight checklist published by Wush covers the accountability structures that regulators examine first.

Pro Tip: Treat your risk framework as a living operating model, not a document. Continuous adaptation is what separates frameworks that produce real governance outputs from those that collect dust between audits.

How do emerging technologies and regulations shape risk frameworks?

Regulatory developments and technological advances are reshaping financial technology risk strategies at the same time, and from both directions. Regulations drive adoption of digital tools. Digital tools, in turn, make compliance more precise and less expensive.

Three regulatory developments define the current environment:

- DORA mandates operational resilience testing, ICT incident classification, and third-party oversight for all EU financial entities. It sets a new baseline for what “adequate” risk governance means.

- MiCAR (Markets in Crypto-Assets Regulation) introduces licensing and disclosure requirements for crypto asset service providers, forcing risk frameworks to address asset-specific exposures that traditional ERM models never anticipated.

- The EU AI Act creates risk tiers for AI systems used in financial services, requiring conformity assessments for high-risk applications like credit scoring and fraud detection models.

On the technology side, blockchain-based finance introduces programmatic risks requiring automated cryptographic verification methods, such as circuit breakers monitoring suspicious mempool transactions. Traditional human-dependent controls cannot operate at the speed or scale that on-chain activity demands.

The relationship between regulation and digitalization runs in both directions. Regulations like Basel III and IFRS 9 drove adoption of AI and cloud tools that improved reporting accuracy and lowered risk parameters. Advanced analytics and machine learning now improve risk parameter accuracy in ways that manual processes cannot match. The regulatory compliance readiness challenge for 2026 is integrating these tools into frameworks that regulators can audit, not just deploying them for internal efficiency.

Digital finance governance also faces the core challenge of balancing innovation with investor protection. Regulatory sandboxes and innovation hubs provide controlled environments where new financial products can be tested without full regulatory exposure. That balance is not a philosophical question. It is a framework design question, and the organizations that answer it well gain a competitive advantage.

Key takeaways

Risk frameworks in digital finance are operational infrastructure, not compliance documentation, and their value is measured by the governance outputs they produce under regulatory scrutiny.

| Point | Details |

|---|---|

| Frameworks define governance structure | Board oversight, accountability, and escalation protocols are the non-negotiable pillars of any credible digital finance framework. |

| Data breach costs justify investment | At $4.44 million globally per incident, the cost of inadequate risk governance exceeds the cost of building a proper framework. |

| Framework layering is standard practice | Most mature organizations combine COSO ERM, ISO 31000, and NIST RMF to cover strategic, operational, and information security risks together. |

| DORA sets the new baseline | EU-regulated entities must treat ICT third-party oversight and incident reporting as core framework requirements, not optional enhancements. |

| Continuous review is mandatory | Frameworks reviewed only annually or after incidents lose their governance value. Automated monitoring and regular third-party audits are the standard. |

Why risk frameworks are not what most finance teams think they are

Most finance teams I have worked with treat risk frameworks as a compliance deliverable. They build them to satisfy an audit, file them, and revisit them when the next audit cycle begins. That approach produces documentation, not governance.

The frameworks that actually protect organizations are the ones that generate real outputs on a defined schedule. Board reports that reference specific risk scores. Escalation logs that show decisions were made and documented. Third-party audit findings that get tracked to closure. The framework is the mechanism that produces those outputs, not the output itself.

The most common failure I see is the integration gap. Financial risk sits with the CFO’s team. Operational risk sits with the COO. Compliance risk sits with the legal function. Nobody owns the intersection, and that is exactly where digital finance incidents originate. A crypto custody failure is simultaneously an operational risk event, a compliance event, and a financial risk event. If your framework cannot process it as all three simultaneously, your escalation will be slow and your response will be fragmented.

The organizations that handle this well treat their enterprise risk management function as the connective tissue between those silos. They use a corporate credibility framework to ensure that risk governance outputs are visible to regulators before a crisis forces the conversation. That visibility is not just good governance. It is a competitive signal to counterparties, investors, and regulators that the organization is serious about digital finance.

My honest outlook: AI and blockchain will not simplify risk frameworks. They will make them more complex and more consequential. The organizations that invest in framework maturity now will spend less time in regulatory remediation later.

— Gregg

Benchmark your digital asset risk readiness with DARE

Finance professionals and compliance teams building or reviewing their digital finance risk frameworks need more than a checklist. They need a structured, independent benchmark that tells them where their governance actually stands.

Wush offers the Digital Asset Readiness Evaluation, known as DARE, a certification program built specifically for enterprise digital asset governance. DARE covers custody, regulatory compliance, risk management, legal controls, and operational resilience in a modular format with annual renewal to keep credentials current as regulations evolve. For teams working through digital asset operational risk challenges, DARE provides the structured framework assessment that internal reviews cannot replicate. Explore the DARE certification to benchmark your organization’s digital finance risk posture against the 2026 standard.

FAQ

What is the role of risk frameworks in digital finance?

Risk frameworks in digital finance provide a structured methodology to identify, assess, mitigate, and monitor financial, operational, and compliance risks. They connect enterprise strategy to regulatory requirements and produce the governance outputs that regulators and auditors examine.

Why is DORA significant for digital finance risk management?

DORA, applied across the EU from january 2025, mandates ICT third-party contract registers, unified incident reporting, and operational resilience testing. It sets a new minimum standard for risk governance in digital finance that affects banks, fintechs, and crypto asset service providers.

How do COSO ERM and ISO 31000 differ in digital finance applications?

COSO ERM connects risk directly to strategic business objectives, making it the preferred choice for boards and executive teams. ISO 31000 provides flexible governance principles that apply across any industry, and most organizations use it as the overarching structure within which COSO ERM or NIST RMF operates.

What makes blockchain risk management different from traditional finance risk?

Blockchain-based finance introduces programmatic risks that require automated cryptographic verification methods rather than human-dependent controls. Circuit breakers monitoring suspicious mempool transactions are one example of the real-time automated approaches that on-chain environments demand.

How often should digital finance risk frameworks be reviewed?

Risk frameworks should be reviewed at least annually and after any material incident or significant regulatory change. Automated monitoring tools and third-party audits between formal reviews maintain the continuous governance posture that regulators expect in 2026.