Digital Asset Fiduciary Responsibility: A 2026 Guide

Digital asset fiduciary responsibility is the legal and ethical duty to manage cryptocurrency, tokenized securities, and other digital property with the same care, loyalty, and prudence required of any fiduciary, while meeting the specialized compliance demands of blockchain-based assets. The Revised Uniform Fiduciary Access to Digital Assets Act (RUFADAA) governs how fiduciaries in most U.S. states may lawfully access and administer these assets. Finance professionals and corporate executives managing digital wealth in 2026 face a compliance environment where platform restrictions, private key security, and anti-money laundering (AML) obligations create risks that traditional asset management frameworks were never designed to address.

What is digital asset fiduciary responsibility under current law?

Digital asset fiduciary responsibility sits at the intersection of fiduciary law and digital property rights. The core obligation is unchanged from traditional fiduciary duty: act in the best interest of the beneficiary, avoid conflicts, and exercise reasonable care. What changes is the legal infrastructure and technical execution required to fulfill that duty.

RUFADAA has been adopted by most U.S. states, enabling fiduciary access only when the principal has granted explicit authorization in advance. Without that authorization, a fiduciary may hold full legal authority over a person’s physical estate yet remain completely locked out of their Bitcoin wallet or exchange account. That gap is not a technicality. It is a structural failure that exposes beneficiaries to real asset loss.

Platform Terms of Service can block fiduciary access even when fiduciary status is legally established. Standard fiduciary powers do not override restrictive digital platform agreements. This means a trustee acting in good faith can still be denied access by Coinbase, Kraken, or any other custodial platform if the account holder never granted explicit RUFADAA-compliant authorization.

Key legal instruments that must address digital asset access include:

- Wills and revocable trusts: Must explicitly authorize the executor or trustee to access, manage, and distribute digital assets.

- Powers of attorney (POA): Must include specific digital asset language referencing RUFADAA, not just broad financial authority.

- Online tool designations: Platforms like Google and Facebook offer native legacy tools that can override estate documents if completed first.

- Private key documentation: Self-custody assets require documented recovery phrases stored securely and accessible to the authorized fiduciary.

Authorization must be established in legal documents before it is needed. Attempting to obtain access after the fact through courts or platform appeals routinely fails.

What are the specific duties of a digital asset fiduciary?

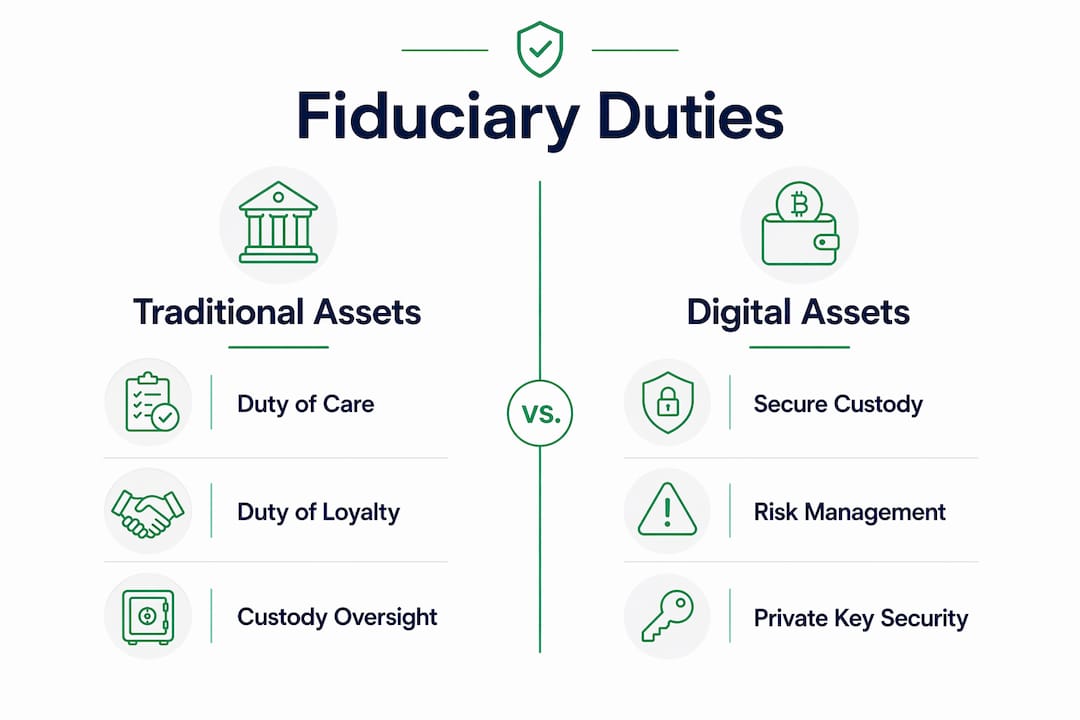

Digital asset fiduciary duty extends beyond investment advice to include secure custody, diligent risk management, and transparent disclosure of conflicts. Each traditional fiduciary duty takes on a distinct technical dimension when applied to digital assets.

Duty of care

The duty of care requires fiduciaries to act with the competence a reasonably prudent professional would apply. For digital assets, that means understanding blockchain transaction finality, smart contract risk, and the operational differences between custodial and self-custody arrangements. A fiduciary who delegates custody to a third-party provider without conducting due diligence on that provider’s security controls and financial stability has breached this duty.

Duty of loyalty

The duty of loyalty prohibits fiduciaries from placing their own interests above those of the beneficiary. In digital asset contexts, this includes disclosing any financial relationship with custodians, exchanges, or DeFi protocols used in managing the portfolio. Undisclosed referral arrangements with crypto platforms are a clear breach.

Duty of prudence

Prudence in digital asset management requires quantitative risk controls. Institutional managers must now apply portfolio volatility analysis and counterparty creditworthiness assessments to digital asset holdings, not just qualitative judgment. A fiduciary who holds an undiversified position in a single volatile token without documented risk analysis cannot claim prudent management.

Private key security

Self-custody crypto assets require private key security comparable to bearer bonds. Recovery without the private key is impossible. No court order, no platform appeal, and no technical workaround can recover assets from a wallet whose keys are lost. Fiduciaries must treat recovery phrases with the same rigor applied to physical bearer instruments: documented, secured, and accessible only to authorized parties.

Pro Tip: Store recovery phrases in a fireproof, tamper-evident physical vault with a documented chain of custody. Never store them digitally on the same network as the assets they protect.

Failure to uphold these duties carries serious consequences. Civil lawsuits and regulatory penalties are the documented outcomes of fiduciary breaches in digital asset management. Reputational damage compounds the financial exposure, particularly for institutional trustees managing client portfolios.

How do digital asset duties differ from traditional asset management?

The fundamental fiduciary duties are the same. The execution is not. Finance professionals who have managed equities, bonds, and real estate for decades will find that digital assets require a different operational model at nearly every step.

| Dimension | Traditional assets | Digital assets |

|---|---|---|

| Custody | Bank or broker holds assets; SIPC or FDIC protection applies | Custodial or self-custody; no federal deposit insurance |

| Access | Court orders and legal authority reliably grant access | Platform Terms of Service and key loss can block access entirely |

| Recovery | Lost certificates can be reissued; courts can compel transfer | Lost private keys are permanently unrecoverable |

| Valuation | Established market prices; regulated exchanges | High volatility; price manipulation risk on unregulated venues |

| Oversight | SEC, FINRA, OCC regulatory frameworks | Fragmented regulation; AML obligations vary by jurisdiction |

| Technical expertise | Legal and financial knowledge sufficient | Blockchain, smart contract, and cybersecurity knowledge required |

Professional trustees should treat digital assets like alternative assets, using a phased, policy-led approach with forensic recovery and cybersecurity support built into the governance model. That framing is useful because it places digital assets in a category finance professionals already know how to manage with elevated scrutiny, rather than treating them as a novel problem requiring entirely new frameworks.

The decentralized nature of many digital asset platforms removes the centralized oversight that traditional fiduciaries rely on. There is no transfer agent to call, no registrar to verify ownership, and no clearing house to reverse an erroneous transaction. Every operational decision is final in a way that traditional asset management is not.

What practical steps should fiduciaries take in 2026?

Many institutional managers struggle to translate high-level fiduciary duties into operational frameworks for digital assets. The steps below address that gap directly.

-

Establish explicit legal authorization. Update all estate planning documents, trusts, and powers of attorney to include RUFADAA-compliant language authorizing digital asset access. Generic financial authority clauses do not cover digital assets on most platforms.

-

Build a complete digital asset inventory. Document every wallet address, exchange account, DeFi position, and NFT holding. Include the platform, approximate value, custody type, and access credentials location. Review and update the inventory at least quarterly.

-

Implement segregated custody protocols. Separate hot wallets used for active transactions from cold storage used for long-term holdings. Apply multi-signature authorization requirements for any transaction above a defined threshold.

-

Conduct custodian due diligence. Evaluate third-party custodians on security certifications (SOC 2 Type II is the current standard), insurance coverage, regulatory standing, and financial stability. Document the evaluation process and repeat it annually.

-

Apply quantitative risk controls. Run portfolio volatility analysis on digital asset positions. Set concentration limits. Assess counterparty creditworthiness for any DeFi protocol or exchange holding client assets.

-

Meet AML and regulatory reporting obligations. Digital asset transactions above reporting thresholds trigger Bank Secrecy Act obligations. Fiduciaries must maintain transaction records, conduct know-your-customer (KYC) checks on counterparties, and file Suspicious Activity Reports (SARs) where required.

-

Pursue formal compliance assessment. Digital asset readiness evaluations provide a structured method for identifying gaps in legal authorization, custody security, and risk management before a breach occurs.

Pro Tip: Treat your digital asset inventory as a living document, not a one-time exercise. Wallet addresses change, DeFi positions expire, and exchange accounts get frozen. A stale inventory is nearly as dangerous as no inventory at all.

Fiduciaries managing institutional portfolios should also review the board-level oversight checklist to confirm that governance structures match the risk profile of the digital asset holdings. Board visibility into custody arrangements, key management, and AML controls is not optional for institutional fiduciaries.

Key Takeaways

Digital asset fiduciary responsibility requires explicit legal authorization, technical custody controls, and quantitative risk management that traditional asset frameworks do not provide on their own.

| Point | Details |

|---|---|

| Legal authorization is non-negotiable | RUFADAA-compliant language must appear in wills, trusts, and POAs before access is ever needed. |

| Private key loss is permanent | Treat recovery phrases like bearer bonds: physically secured, documented, and accessible only to authorized fiduciaries. |

| Platform terms override legal authority | Standard fiduciary powers do not override restrictive exchange or wallet platform agreements. |

| Quantitative risk controls are now required | Portfolio volatility analysis and counterparty creditworthiness assessments are part of the prudence standard for digital assets. |

| Compliance gaps require structured assessment | Formal readiness evaluations identify legal, custody, and operational failures before they become breaches. |

The compliance gap most fiduciaries underestimate

The most common mistake I see among experienced fiduciaries entering the digital asset space is assuming that legal authority is the same as practical access. It is not. A trustee can hold a court-certified letter of appointment and still be denied access to a Coinbase account because the deceased never completed the platform’s legacy access tool. That is not a legal failure. It is an operational one, and it happens constantly.

The second mistake is confusing digital asset management in the IT or marketing sense with digital asset fiduciary responsibility in the legal and financial sense. These are entirely different disciplines. A firm that manages its brand’s digital content library has no relevant experience managing a client’s tokenized securities portfolio. Finance professionals need to be clear about which domain they are operating in.

What I find encouraging is the emergence of structured frameworks that treat digital assets as a distinct asset class requiring its own governance layer. The phased, policy-led approach that professional trustees are beginning to adopt mirrors how institutional managers first approached hedge funds and private equity: with elevated scrutiny, documented due diligence, and clear board-level accountability. That is the right model. The legal risk management guide from Wush captures much of this thinking in a format that translates directly into institutional practice.

The fiduciaries who will avoid liability in the next five years are the ones who treat digital asset compliance as a continuous process, not a one-time legal review. Annual reassessment, updated inventories, and ongoing custodian due diligence are the baseline. Everything else builds from there.

— Gregg

Wush DARE: a readiness framework built for digital fiduciaries

Finance professionals who recognize the compliance gaps described in this article need more than awareness. They need a structured way to measure where they stand and what to fix.

Wush offers the Digital Asset Readiness Evaluation (DARE), an independent certification designed specifically for fiduciaries, treasury teams, legal advisors, and risk managers operating in the digital asset space. DARE covers custody security, regulatory compliance, legal authorization, AML controls, and operational risk in a modular assessment format with annual renewal. The credential is blockchain-verified and recognized as an industry standard for enterprise digital asset governance. For fiduciaries who need to demonstrate due diligence to boards, regulators, or beneficiaries, DARE provides the documented framework to do it. Learn more at dare.wush.co.

FAQ

What is digital asset fiduciary responsibility?

Digital asset fiduciary responsibility is the legal and ethical duty to manage cryptocurrency and other digital property with care, loyalty, and prudence on behalf of a beneficiary. It requires explicit legal authorization, secure custody protocols, and compliance with frameworks like RUFADAA.

Does RUFADAA apply in every U.S. state?

RUFADAA has been adopted by most U.S. states, but not all. Fiduciaries must verify whether their state has enacted RUFADAA and confirm that estate documents include the specific language the law requires for digital asset access.

Can a fiduciary access digital assets without advance authorization?

No. Without explicit authorization in estate planning documents, platform Terms of Service and privacy laws routinely block fiduciary access regardless of legal standing. Authorization must be established before it is needed.

What happens if a private key is lost?

Private key loss is permanent. No court order or technical recovery method can restore access to a self-custody wallet without the original key or recovery phrase. Fiduciaries must document and secure recovery phrases with the same rigor applied to bearer bonds.

What certifications help fiduciaries meet digital asset compliance standards?

The DARE certification from Wush is an industry-recognized credential covering custody, legal compliance, AML obligations, and operational risk management for fiduciaries managing digital assets in enterprise environments.