Digital Asset Accounting Standards Explained for Finance Teams

Digital asset accounting standards are the rules governing how enterprises classify, measure, and disclose cryptocurrency holdings and related tokens in financial statements under IFRS and US GAAP. These standards determine whether Bitcoin sits on your balance sheet as an intangible asset, inventory, or financial instrument, and that classification drives everything from impairment testing to earnings volatility. With FASB ASU 2023-08 now effective and IFRS interpretations continuing to evolve, finance professionals and corporate executives need precise command of these frameworks. Getting the classification wrong is not a technical footnote. It is an audit finding.

What are the key classification categories for digital assets under IFRS and US GAAP?

Digital asset accounting standards explained at their most foundational level require you to answer one question first: what is this asset, and how does the business use it? The answer determines every subsequent accounting decision.

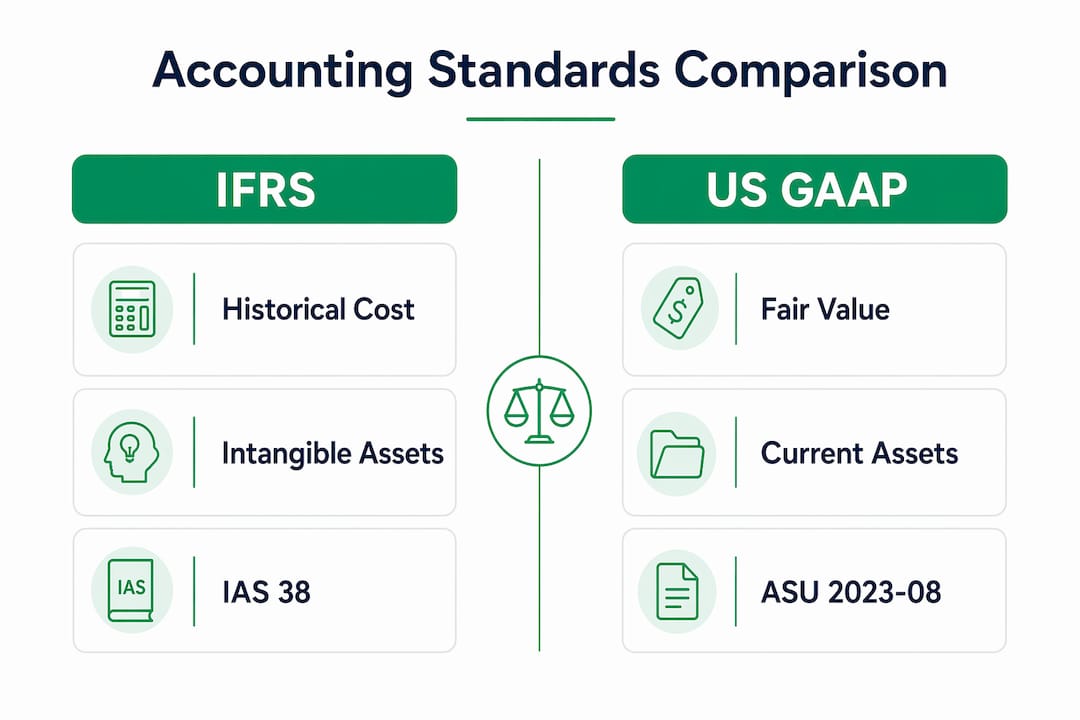

Under IFRS, the default classification is intangible assets under IAS 38. Cryptocurrencies fall here unless the entity’s rights or business model indicate otherwise. The cost model applies by default, meaning you record at acquisition cost and test for impairment annually. The revaluation model is available only when an active market exists, which allows carrying value to reflect current prices but routes gains through other comprehensive income rather than profit or loss.

Two significant exceptions break from the IAS 38 default:

- Broker-trader inventory: Entities that buy and sell digital assets in the ordinary course of business must classify crypto as inventory under IAS 2, measured at fair value less costs to sell. Changes flow directly through profit or loss, which materially changes income statement presentation compared to IAS 38 treatment.

- Financial instruments: Tokens that carry contractual rights, such as debt-like tokens or certain stablecoins with redemption rights, may qualify as financial instruments under IFRS 9. This classification triggers fair value through profit or loss or amortized cost measurement depending on the business model test.

Under US GAAP, FASB introduced Subtopic ASC 350-60 specifically for crypto assets. To qualify for inclusion, an asset must meet four criteria: it must be an intangible asset, secured through cryptography, exist on a distributed ledger, and not grant the holder a claim on goods, services, or another financial instrument. Bitcoin and Ether qualify. Most utility tokens and stablecoins do not, and they fall back to other ASC guidance.

Wrapped tokens present a particular challenge. A wrapped version of Bitcoin, for example, may carry different contractual characteristics than the underlying asset, requiring separate classification analysis. FASB has proposed expanding Subtopic 350-60 to address wrapped token classification explicitly, with guidance expected to affect compliance from 2026 onward.

Pro Tip: Build a token-by-token classification register before your next reporting cycle. A blanket policy that treats all digital assets identically will not survive audit scrutiny when your portfolio contains Bitcoin, a governance token, and a stablecoin.

How are digital assets measured and presented in financial statements?

Measurement rules differ sharply between IFRS and US GAAP, and the gap has widened since FASB’s 2023 update. Understanding both frameworks is necessary for any multinational enterprise or company considering a dual-reporting environment.

| Framework | Measurement basis | Gains and losses |

|---|---|---|

| IFRS IAS 38 (cost model) | Historical cost less impairment | Impairment losses through P&L; no upward reversal to P&L |

| IFRS IAS 38 (revaluation model) | Fair value when active market exists | Gains through OCI; losses through P&L |

| IFRS IAS 2 (broker-trader) | Fair value less costs to sell | All changes through P&L |

| US GAAP ASC 350-60 (ASU 2023-08) | Fair value at each reporting date | All changes through net income |

FASB’s ASU 2023-08 is the most significant shift in US GAAP crypto accounting to date. In-scope crypto assets must be remeasured at fair value each reporting date, with all gains and losses flowing through net income. This eliminates the previous practice of recording only impairment losses while ignoring recoveries. The practical effect is that a company holding Bitcoin will report unrealized gains in a rising market and unrealized losses in a declining one, directly affecting reported earnings per share.

Fair value measurement under both frameworks requires more than pulling a spot price from an exchange. Under IFRS 13, principal market determination requires analyzing exchange volume and activity across multiple trading venues and documenting the judgment. The principal market is the one with the greatest volume and level of activity for the asset. If no principal market exists, you use the most advantageous market. This analysis must be performed consistently and documented at each measurement date.

Under ASC 820, the US GAAP equivalent, consistent principal market selection and valuation timing are required. Ad hoc spot pricing from whichever exchange is convenient does not meet the standard. Finance teams need a documented policy naming the principal market for each asset class and a process for capturing prices at the measurement date and time.

On the balance sheet, digital assets appear as a separate line item under intangible assets or current assets depending on holding intent. On the income statement, unrealized fair value changes appear as a distinct line under ASU 2023-08. Cash flow statements must classify proceeds from sales as operating or investing activities based on the nature of the holding, which requires consistent policy documentation.

Pro Tip: Earnings volatility from fair value remeasurement is not a bug in ASU 2023-08. It is the intended outcome. Prepare your board and investor relations team with a clear narrative before your first quarterly filing under the new standard.

What are the main disclosure requirements and audit considerations for digital assets?

Disclosure requirements under ASU 2023-08 are specific and demanding. Finance teams that approach this as a checkbox exercise will find themselves revising filings. The standard requires disclosure of the following for each significant digital asset:

- The name and nature of the asset

- Cost basis at the beginning and end of the period

- Fair value at each reporting date

- Units held at each reporting date

- The cost-basis method used (specific identification, FIFO, or average cost)

- Annual rollforward showing additions, disposals, and fair value changes

These disclosure requirements imply detailed portfolio-level tracking across every reporting date and year-end. A spreadsheet updated quarterly is not sufficient infrastructure for a public company or a large private enterprise with material crypto holdings.

IFRS disclosure requirements under IAS 38 and IFRS 13 are less prescriptive but still require disclosure of the accounting policy, the carrying amount, any impairment losses recognized, and the fair value measurement inputs and hierarchy level. Entities using the revaluation model must disclose the effective date of the revaluation, whether an independent valuer was involved, and the revaluation surplus.

Audit considerations add another layer of complexity. Auditors require evidence across four assertions: ownership, valuation, completeness, and disclosure. Audit evidence must go beyond screenshots. Finance teams need comprehensive reconciliation between wallets, ledgers, and financial statements. Specifically, auditors will expect:

- Wallet-to-legal-entity mapping that ties each wallet address to a specific legal entity and custodian

- Valuation support showing the principal market, price source, and measurement time for each asset

- Completeness testing that accounts for all wallets, including cold storage and third-party custodians

- Disclosure tie-out confirming that footnote disclosures match the underlying data

Tax reporting adds a parallel compliance obligation. The IRS treats digital asset sales as taxable whether they generate gains or losses, and new broker reporting requirements under Form 1099-DA take effect in 2025 and 2026. Finance teams must coordinate tax and financial reporting to avoid inconsistencies that create audit risk in both domains.

Pro Tip: Map every wallet address to a legal entity and custodian before your audit begins. Wallet-to-ledger mapping is the single most common gap auditors identify in first-year crypto audits.

How do recent 2025 and 2026 updates affect compliance practices?

The accounting standards for digital assets are not static. Two developments in 2025 and 2026 require immediate attention from finance leaders.

- ASU 2023-08 is now effective for fiscal years beginning after December 15, 2024, meaning calendar-year public companies are reporting under the new fair value standard for the first time in 2025. The transition requires a cumulative-effect adjustment to retained earnings as of the adoption date, with prior periods not restated.

- FASB’s proposed scope expansion extends Subtopic 350-60 to wrapped tokens and stablecoin guidance, with stablecoins potentially qualifying as cash equivalents when backed by high-quality reserves and offering on-demand redemption. This classification would move stablecoins off the intangible asset line and onto the cash and cash equivalents line, a material balance sheet change.

- Stablecoin cash equivalent classification requires documented evidence of reserve quality and redemption rights. Documented high-quality reserves and on-demand redemption rights are the threshold conditions. Holding a stablecoin without reviewing the issuer’s reserve attestations is no longer defensible accounting practice.

- Operational infrastructure gaps are the primary implementation risk. Fair value measurement under ASC 820 and IFRS 13 requires consistent, documented, and auditable pricing processes. Many finance teams that relied on manual processes for a small crypto position are now facing material holdings that require institutional-grade data infrastructure.

- Internal controls over digital asset reporting must be designed and tested as part of SOX compliance for US public companies. Controls over wallet access, transaction authorization, fair value pricing, and disclosure preparation are all in scope.

The governance gap in enterprise digital asset operations is real. A governance gap assessment conducted before your next audit cycle will surface control deficiencies before your auditors do.

Key takeaways

Digital asset accounting standards require token-level classification under IFRS and US GAAP, with measurement and disclosure obligations that demand institutional-grade data infrastructure and documented internal controls.

| Point | Details |

|---|---|

| Classification drives everything | Each token requires individual analysis under IAS 38, IAS 2, IFRS 9, or ASC 350-60 based on rights and business model. |

| ASU 2023-08 changes US GAAP materially | Fair value remeasurement at each reporting date flows all gains and losses through net income, creating earnings volatility. |

| Disclosure requirements are granular | ASU 2023-08 requires name, cost basis, fair value, units held, cost-basis method, and annual rollforward per asset. |

| Audit evidence requires full reconciliation | Wallet-to-ledger mapping, principal market documentation, and completeness testing are the core audit evidence requirements. |

| 2025 and 2026 updates expand scope | Wrapped tokens and stablecoins face new classification guidance that may shift balance sheet presentation significantly. |

The classification problem nobody talks about enough

Most finance teams I work with approach digital asset accounting as a single policy problem. They want one rule that covers everything. That instinct is understandable, but it is the wrong frame entirely.

The reality is that a single enterprise treasury can hold Bitcoin under ASC 350-60, a governance token that falls outside that scope entirely, and a stablecoin that may qualify as a cash equivalent under proposed FASB guidance. Three assets, three different accounting treatments, three different disclosure requirements. A blanket policy does not just fail audit scrutiny. It produces financial statements that misrepresent the economic reality of the portfolio.

The second problem I see consistently is underinvestment in data infrastructure. Fair value measurement under ASC 820 and IFRS 13 is not a quarterly exercise you can complete with a spreadsheet and a screenshot from Coinbase. It requires a documented principal market, a consistent pricing methodology, and a timestamp-accurate price capture process. Finance teams that built their crypto accounting process when holdings were immaterial are now finding that the same process cannot support a material position under audit.

The third issue is the coordination gap between financial reporting and tax. The IRS treats every disposal as a taxable event, and Form 1099-DA broker reporting is now live. If your tax team and your financial reporting team are not using the same cost-basis methodology and the same transaction records, you will have inconsistencies that create exposure in both domains.

The finance leaders who navigate this well are the ones who treat digital asset accounting as a discipline requiring dedicated infrastructure, not an extension of existing intangible asset processes.

— Gregg

How DARE helps finance teams meet accounting and audit standards

Finance teams facing their first audit under ASU 2023-08 or preparing for IFRS disclosure reviews need more than general guidance. They need a structured framework that maps directly to the control and documentation requirements auditors expect.

Wush’s DARE certification is built specifically for this challenge. The Digital Asset Readiness Evaluation covers custody controls, fair value measurement processes, disclosure completeness, and audit traceability across the full digital asset portfolio. It gives finance professionals and executives a structured way to assess where their controls meet the standard and where gaps remain. The annual renewal process keeps your team current as FASB and IFRS guidance continues to evolve. If your organization holds digital assets and faces a financial statement audit, the DARE framework provides the compliance edge that separates a clean audit from a qualified one.

FAQ

What is the default IFRS classification for cryptocurrencies?

Under IFRS, cryptocurrencies are classified as intangible assets under IAS 38 by default. Exceptions apply for broker-traders, who classify holdings as inventory under IAS 2, and for tokens with contractual rights that qualify as financial instruments under IFRS 9.

What does FASB ASU 2023-08 require for crypto asset measurement?

ASU 2023-08 requires in-scope crypto assets to be remeasured at fair value at each reporting date, with all gains and losses recognized through net income. The standard is effective for calendar-year public companies beginning in 2025.

What disclosures are required under ASU 2023-08?

Entities must disclose the asset name, cost basis, fair value, units held, cost-basis method, and an annual rollforward for each significant digital asset. This requires portfolio-level tracking infrastructure, not manual spreadsheets.

Can stablecoins be classified as cash equivalents?

FASB’s proposed guidance allows stablecoin classification as cash equivalents when the issuer maintains high-quality reserves and offers on-demand redemption rights. Finance teams must document reserve quality and redemption terms to support this classification.

What audit evidence do finance teams need for digital assets?

Auditors require wallet-to-legal-entity mapping, principal market documentation for fair value, completeness testing across all wallets and custodians, and disclosure tie-outs. Screenshots alone do not satisfy audit evidence standards under either IFRS or US GAAP.